Worldyards Monthly Newsletter

|

|

|

- Gabriella Carson

- 6 years ago

- Views:

Transcription

1 October Worldyards Monthly Newsletter This is a monthly publication of Worldyards which summarizes developments in the newbuilding market in the past month with a special focus on shipbuilders. We start with a summary table, followed by shipbuilding output forecast and newbuilding price index. We then list the newbuilding orders, present our statistical summaries on terminations, slippage/advancement, rescheduling and demolitions, and conclude the newsletter with latest developments in shipbuilders, their host countries and shipbuilding technology. For latest figures on orderbook ratio, age profile and delivery schedule of various segments and other vital statistics, log onto our website ( Summary of Orders and Investments, Oct New Contracts Investment (USD Million) Bulkers 6,771,900 (+94%) 2, (+106%) Containers 19,100 Nominal TEU (-85%) (-80%) Semi-liner Tonnage 115,000 (+80%) 125 (+64%) LNG (Gas I) 600,000 CBM n/a 850 n/a LPG (Gas III) 244,000 CBM (-34%) 346 (-33%) Product Tanker 652,000 (+23%) (+8%) Product/Chemical Tanker 1,488,592 (+1,235%) 966 (+998%) Chemical Tanker 360,000 (+109%) (+58%) Passenger Ships 130,000 GT n/a n/a Notes: (1) %: It is the percentage change over last month. (2) Percentage numbers are rounded up. (3) There were no LNG (Gas I) and Passenger Ships) in September, therefore no comparison percentage to current month. (4) Please refer to Worldyards segment definitions listed in the Member site for detailed explanations for the segments. Page 1 of 21

2 Shipbuilding Capacity and Utilization Year Capacity Annual Delivery Scheduled Delivery Capacity / (CGT) Growth (CGT) (CGT) Utilization ,782,340-40,366, % ,063, % 41,563, % ,632, % 47,561, % ,180, % 46,389, % ,549, % 45,544, % 74,628, % 28,843,424 11,995, % ,414, % 81,231 33,952, % ,005, % - 25,069, % 80,878, % - 11,185, % ,304, % - 1,360, % * Stale orders (please refer to Key Statistics -> Orderbook -> Scheduled Deliveries for the definition of stale orders) Worldyards shipbuilding capacity and utilization estimate is not a result of mathematical forecast, but rather result of a sum-of-all-parts approach estimating micro developments in each and every shipbuilder. First, Worldyards assumed 2008 as the base for maximum capacity or full utilization except for the few builders who have just started production in mid to end of 2007 and a number of builders who have delivered more in (Please note that our previous capacity calculation is essentially based on the builder's output. For the detailed discussion see our market comment dated on 23 June 2010, Utilisation as a Metric of Shipbuilding Capacity). Then, we assume an organic productivity growth of 3 5% for each shipbuilder annually. The organic baseline of 3-5% depends on the status of the market and the country of the builder. We use 5% for good market, 3% for less good market. However productivity can be reduced also if a builder produces consistently below their potential in depressed market, they will slow down investment for technical and technological improvements, lay off workers, and take on a more diverse product mix than what is ideal for productivity. So we assume -3% for each year where output is 15% below potential for the previous year, -5% if the output gap is bigger than 15%. On top of the organic growth (or decline), the growth rate is then adjusted upwards or downwards to allow for other productivity developments (we call them "capacity-significant events"), caused by events such as new production methods/processes, introduction of facilities/equipment, closure of facilities, shifting of strategic focus from merchant shipbuilding to other activities, etc. Worldyards evaluates each event and assess their impact which will be added on or subtracted from the 3 5% baseline growth rate for each shipbuilder. Each and every of these capacity-significant events can be viewed under the "Background" box of each shipbuilders in the member site. For any additional facility of the shipbuilder, the increment capacity will be distributed as 60% on its first year of production, another 25% on its second year (or 85% in total) and full production on its third year (capacity will Page 2 of 21

3 reach its designed level in 3 years). On the other hand, for any closure of facility, full capacity will be deducted upon its effectivity year since we can't close a drydock/facility gradually. The Worldwide, Continent-wise and Country-wise estimates are just a summation of resultant estimates of individual builders. It is important to note though that "available capacity" would appear much higher due to the fact that the Japanese orderbook is significantly under-reported, our solution to this is to create "proforma orders" for some yards as deemed appropriate. Page 3 of 21

4 New Orders The order is defined as a confirmed signed contract in Worldyards. Every effort has been made to confirm the order. LOIs are excluded. Options declared are treated as new orders. Sub-Segment Capacity Shipbuilder Delivery Beneficial Owner Handysize Handysize Handysize Handysize 2 x 37,600 5 x 38,500 8 x 38,500 4 x 39,200 Price (US $ M) Imabari 2015 Wisdom Marine 24 Huatai Heavy Shanhaiguan Shipbuilding Zhejiang Ouhua Interlink Maritime Dalian Tiger Shipping China Navigation 22.5* 22.5* 22.5* Date 25-Oct- 15-Oct- 30-Oct- 11-Oct- 55,000 2 x 60,200 4 x 61,000 2 x 61,000 3 x 64,000 6 x 64,000 2 x 64,000 Kawasaki Heavy Industries Mitsui, MES Imabari Jun-2015 Wisdom Marine 27 NACKS Chengxi Shipyard China Shipping Industry (Jiangsu) Jiangsu Hantong 2015 Scorpio Bulkers [Scorpio Group] Scorpio Bulkers [Scorpio Group] Scorpio Bulkers [Scorpio Group] Scorpio Bulkers [Scorpio Group] Tomini Ship Management HI Investment & Securities 30* 30* 28.5* 27* Oct- 7-Oct- 7-Oct- 7-Oct- 7-Oct- 20-Oct- 25-Oct- Panamax Bulker Panamax Bulker Panamax Bulker Panamax Bulker Panamax Bulker 2 x 77,000 2 x 77,000 2 x 82,000 5 x 82,000 6 x 82,000 Sasebo Shipyard 2015 Santoku Senpaku 31* Sasebo Shipyard Hanjin Heavy Jiangsu Hantong Shanghai Shipyard Safe Bulkers 30 Hyundai Merchant Marine, HMM 26.3 Nisshin Shipping 28* 2015 Scorpio Tankers [Scorpio Group] 28* 21-Oct- 31-Oct- 22-Oct- 26-Oct- 28-Oct- Capesize Capesize Capesize Capesize Capesize Capesize 4 x 180,000 2 x 180,000 2 x 180,000 2 x 180, ,000 4 x 208,000 Shanghai Waigaoqiao, SWS Hanjin Heavy 2015 Hanjin Heavy 2015 New Times, NTS Hanjin Heavy Yangzijiang Shipbuilding Zhejiang Herun 54 Feb- Golden Union Shipping Ciner Shipping [Ciner Group] Frontline 50 Poseidon Shipping Oldendorff Carriers [Egon Oldendorff] * 15-Oct- 23-Oct- 25-Oct- 25-Oct- 31-Oct- 7-Oct- Page 4 of 21

5 Sub-Segment Capacity Shipbuilder Delivery Beneficial Owner Capesize 2 x 208,000 Taizhou CATIC Oldendorff Carriers [Egon Oldendorff] Price (US $ M) 54* Date 21-Oct- Containership 1,000-1,499 teu 2 x 1,450 Nominal TEU Brodosplit Shipyard 2015 n/a 20* 18-Oct- Containership 1,500-1,999 teu 4 x 1,800 Nominal TEU CSBC Corporation SITC 23 1-Oct- Containership 7,000-9,999 teu 9,000 Nominal TEU HHIC-Phil 31-May NSC Schifffahrt Oct- MPP 5 x 23,000 Taizhou Sanfu 2015 Renjian Group 25* 14-Oct- Conventional LNG 4 x 150,000 CBM Hyundai Heavy, HHI / 2017 Petronas Oct- LPG 0-9,999 cbm 2 x 5,000 CBM Kitanihon 2015 Brave Maritime [Vafias Group] 19* 7-Oct- LPG 10,000-19,999 cbm LPG 10,000-19,999 cbm 2 x 11,000 CBM 2 x 11,000 CBM Kyokuyo Shipyard 2015 Petredec 28.5* Sasaki Shipyard 2015 Petredec Oct- 2-Oct- LPG 20,000-29,999 cbm 22,000 CBM Jiangnan Shipyard (Group) Dec-2015 Navigator Holdings Oct- VLGC 2 x 84,000 CBM Hyundai Heavy, HHI Scorpio Tankers [Scorpio Group] Oct- MR 4 x 50,000 Sungdong Shipbuilding A.P. Moller - Maersk Oct- LR II 4 x 113,000 Guangzhou Longxue Navig Oct- MR/Chemical MR/Chemical MR/Chemical MR/Chemical 4 x 39,000 8 x 49,999 6 x 52, x 52,000 Hyundai - Vinashin Guangzhou Shipyard International, GSI Hyundai Mipo, HMD Hyundai Mipo, HMD d'amico Tankers [d'amico Group] 31.2 Tankers Inc. 35* Middle Eastern 30.7 Middle Eastern Oct- 23-Oct- 29-Oct- 29-Oct- Page 5 of 21

6 Sub-Segment Capacity Shipbuilder Delivery Beneficial Owner Chemical 20,000-39,999 dwt Chemical 20,000-39,999 dwt 6 x 37,000 38,000 Hyundai Mipo, HMD Hudong- Zhonghua 2015 Feb-2017 Navig8 Chemical Tankers NYK Stolt Tankers Price (US $ M) * Date 8-Oct- 29-Oct- Chemical 40,000-80,000 dwt 2 x 50,000 Samjin Shipbuilding, SSI 2015 Anglo-Atlantic Steamship 35* 7-Oct- Cruise ship 130,000 GT Meyer Werft * WY Estimates 12-Oct- Chinese Dream Oct- Resale Sub-Segment Capacity Shipbuilder Seller Buyer 63,500 63,500 Dayang Shipbuilding Dayang Shipbuilding Crown Ship Ltd. [Sinopacific] Crown Ship Ltd. [Sinopacific] Price (US $ M) German 26 Greek 26 Date 01-Oct- 01-Oct- Panamax Bulker Panamax Bulker Panamax Bulker Panamax Bulker 2 x 81,600 82,100 82,000 2 x 84,000 Tsuneishi Zhoushan Tsuneishi Shipbuilding Jiangsu Hantong Imabari Wisdom Marine Group Mardas Marmara Deniz Isletmeciligi AS (Mardas Shipping Management Co Inc) Ji Mei Hua Shipping Wisdom Marine Group Scorpio Bulkers Inc. [Scorpio Group] 31.5 Greek 31 W Marine Inc Scorpio Bulkers Inc. [Scorpio Group] Oct- 08-Oct- 01-Oct- 07-Oct- Page 6 of 21

7 Newly Surfaced Existing Orders Orders that were placed before the publishing date of our last issue, but only became known to, or were confirmed by Worldyards, after we published our last issue. Some are net additions in number of orders, for instance we only knew of 2 vessels but it has now emerged that there were total 4. Sub-Segment Capacity Shipbuilder Delivery Beneficial Owner Open Hatch Bulk Carriers 2 x 39,000 Zhoushan Changhong 2014 New Yangtze Navigation Price (US $ M) Date 22.5* n/a Small Handy 2 x 15,000 Jiangsu Haitong Offshore 2014 Hengli Petrochemical [Hengli Group] 11* n/a Handysize Handysize Handysize 2 x 27,700 4 x 34,000 2 x 37,000 Dingheng Ship Industry Namura Shipyard Hyundai - Vinashin MST 19* 23-Aug n/a 24* n/a 2014 HI Investment & Securities 24* 15-Apr- 3 x 56,700 4 x 63,500 Hyundai - Vinashin Dayang Shipbuilding n/a 25* 2014 / 2015 Thenamaris 26.5* 15-May- 24-Jan- Panamax Bulker 63,500 Hyundai - Vinashin Panamax Bulker 76,500 Imabari Panamax Bulker Panamax Bulker Panamax Bulker 2 x 82,000 2 x 82,000 2 x 82,000 Jinling Shipyard Jinling Shipyard Jinling Shipyard Dec Mar Joong Ang Shipping Safe Bulkers Cara Shipping 26.5* 2014 / n/a 27* Qingdao Datong Shipping 26.5* n/a 27* 30-Sep- 15-Feb- 15-May- 16-Sep- Capesize 2 x 208,000 Taizhou CATIC Oldendorff Carriers [Egon Oldendorff] 54* 17-Sep- Containership teu 6 x 882 Nominal TEU Taizhou Maple Leaf 2014 Guangxi Yangpu Zhongliang Shipping 8* n/a Containership 7,000-9,999 teu 2 x 9,000 Nominal TEU HHIC-Phil 2015 York Capital Management / Costamare 86* 26-Jul- LPG 0-9,999 cbm 2 x 5,000 CBM Murakami Hide 2014 Geogas Trading 17* n/a LPG 20,000-29,999 cbm 3 x 22,000 CBM Sinopacific Offshore & Engineering Eletson 44* 20-Sep- Page 7 of 21

8 Sub-Segment Capacity Shipbuilder Delivery Beneficial Owner MR/Chemical MR/Chemical MR/Chemical 3 x 50,000 6 x 50,000 4 x 50,300 Hyundai - Vinashin Hyundai Mipo, HMD Price (US $ M) Date Central Mare 35* n/a 2015 American 35* SPP 2015 Vitol 35* 14-Jun- 30-Aug- Chemical 20,000-39,999 dwt 2 x 21,600 Shin Kurushima 2015 MTM Ship Management 39* 30-Sep- Pure Bunker Dingheng Global Energy 4,200 Oct * Tankers Ship Industry (Asia) * WY Estimates Please check our site for details of removed confirmed orders - orders which have become invalid for whatever reasons. 14-Jun- Deals under Negotiation Sub-Segment Capacity Shipbuilder Delivery Beneficial Owner - Price (US $ M) Deductions (in CGT and no. of Orders in bracket) as compared to Orderbook Recorded Page 8 of 21

9 Page 9 of 21

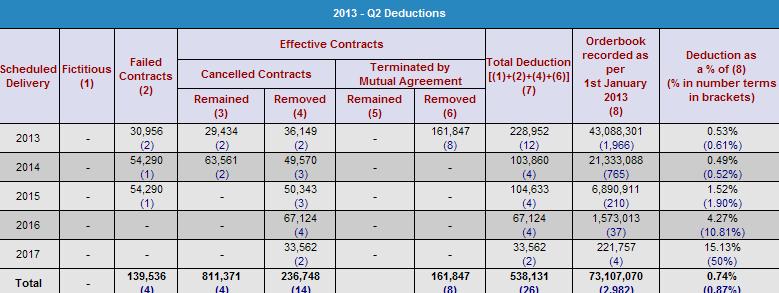

10 Notes: Fictitious Orders: Orders that were never signed but wrongly reported. Theoretically they shall never have been part of the orderbook, even though some of them did find their way in. Some of them even have IMO numbers. Failed order: Signed contracts confirmed to have failed to become effective. We treat terminated orders between shipbuilders and ship-owning companies which are both controlled by the same ultimate interests as failed orders. There are some builders which are operating differently from the normal built-to-order business model they start building vessels on speculation that they could sell them closer to delivery, alternatively they (or the nominal ship-owners within the same group) will offer them for long-term charter. Examples are a lot of the Turkish yards, some Japanese yards such as Imabari and Tsuneishi. Even though they could have nominal shipbuilding contracts, but they can be regarded as internal transfers within the group so the normal contractual relationships regarding installments, refundment guarantees etc. may not apply. The owners will choose to stop construction at anytime of its choice without having to consider the legal obligations under the shipbuilding contract. Whenever we have been able to establish the same ownership interests for the concerned shipbuilder and ship-owning companies, we will treat their terminated contracts as failed. Column (2) & (4) are still part of the orderbook and thus not included on the Total Deduction column, i.e. builder decided to continue construction of the vessels. Cancelled Orders: Effective contracts which have been cancelled legitimately or abandoned by way of defaults. Terminated by Mutual Agreement: An agreement between buyer and shipyard to negate an effective shipbuilding contract, especially those with deliveries in the distant future. The buyers would normally agree to pay the shipbuilders some compensation. Within the shipbuilding contract there are strict mechanisms governing how the contract can be rescinded, this is an extra contractual way to terminate the shipbuilding contract. Page 10 of 21

11 Slippage/Advancement in 2012 Segment Bulkers Containers Semi-liner Tonnage LNG (Gas I) LPG (Gas III) Combination Carriers Crude Tanker Product Tanker Product/Chemical Tanker Chemical Tanker Specialised Tanker Specialised Cargo (Specialised Cargo I) Vehicles Carrier (Specialised Cargo II) Heavy-Lift Cargo (Specialised Cargo III) Passenger Ships Total Unit Scheduled Delivery (as per 1 st January) (a) Ahead of Schedule (b) On-time (c) Realised Confirmed deductions / fictitious (d) Slippage (e) Actual Deliveries No. : (0.76%) 870 (60.08%) 139 (9.60%) 427 (29.49%) 1202 CGT : 27,949, ,248 17,173,778 2,549,807 8,014,465 (0.70%) (61.44%) (9.12%) (28.67%) 22,876,773 No. : (1.52%) 169 (64.26%) 21 (7.98%) 69 (26.24%) 205 CGT : 9,146, ,691 6,129,190 2,424, ,257 (5.10%) (1.39%) (67.01%) (26.50%) 6,827,743 No. : (2.55%) 133 (48.54%) 47 (17.15%) 87 (31.75%) 279 CGT : 2,674,947 57,228 (2.14%) 1,379, , ,200 (17.76%) (51.56%) (28.54%) 2,255,455 No. : 6-2 (33.33%) 0 (0.00%) 4 (66.67%) 2 CGT : 441, , ,338 0 (0.00%) (36.27%) (63.73%) 160,096 No. : 38 1 (2.63%) 20 (52.63%) 5 (13.16%) 12 (31.58%) 37 CGT : 434,851 8,698 (2.00%) 229, ,869 48,200 (11.08%) (52.68%) (34.23%) 354,376 No. : (100.00%) - - CGT : 55, No. : (60.13%) 20 (12.66%) 43 (27.22%) 115 CGT : 5,619,892-3,359,294 1,511, ,648 (13.32%) (59.78%) (26.90%) 4,078,054 No. : (0.83%) 48 (39.67%) 26 (21.49%) 46 (38.02%) 122 CGT : 1,467,847 13,794 (0.94%) 792, , ,423 (19.92%) (54.02%) (25.11%) 1,361,260 No. : (41.12%) 21 (19.63%) 42 (39.25%) 80 CGT : 1,955, , , ,295 (14.08%) (45.62%) (40.31%) 1,331,427 No. : (36.49%) 24 (32.43%) 23 (31.08%) 49 CGT : 1,059, , , ,381 (27.21%) (41.21%) (31.58%) 697,343 No. : (48.48%) 2 (6.06%) 15 (45.45%) 40 CGT : 437, , ,981 19,902 (4.55%) (52.71%) (42.74%) 408,135 No. : 7-1 (14.29%) 2 (28.57%) 4 (57.14%) 4 CGT : 67,470-7,872 (11.67%) 25,145 (37.27%) 34,453 (51.06%) 22,007 No. : (71.11%) 8 (17.78%) 5 (11.11%) 34 CGT : 1,390, , , ,448 (16.72%) (71.45%) (11.83%) 1,051,475 No. : CGT : No. : 7-7 (100.00%) CGT : 815, ,508 (100.00%) ,508 No. : 2, (0.93%) 1,464 (56.70%) 316 (12.24%) 777 (30.09%) 2,176 CGT: 53,516, ,659 32,599,710 5,477,520 15,021,377 (0.75%) (60.91%) (10.24%) (28.07%) 42,239,652 Page 11 of 21

12 Slippage/Advancement in Q1- Segment Bulkers Containers Semi-liner Tonnage LNG (Gas I) LPG (Gas III) Combination Carriers Crude Tanker Product Tanker Product/Chemical Tanker Chemical Tanker Specialised Tanker Specialised Cargo (Specialised Cargo I) Vehicles Carrier (Specialised Cargo II) Heavy-Lift Cargo (Specialised Cargo III) Passenger Ships Total Unit Scheduled Delivery (as per 1 st January) (a) Ahead of Schedule (b) On-time (c) Realised Confirmed deductions / fictitious (d) Slippage (e) Actual Deliveries No. : (1.52%) 140 (35.44%) 19 (4.81%) 230 (58.23%) 257 CGT : 7,523, ,914 2,768,245 4,327, ,354 (4.34%) (1.34%) (36.79%) (57.53%) 4,918,729 No. : (37.97%) 5 (6.33%) 44 (55.70%) 56 CGT : 2,412, ,066 1,206, ,635 (9.35%) (40.66%) (49.99%) 1,942,071 No. : 66 3 (4.55%) 24 (36.36%) 6 (9.09%) 33 (50.00%) 50 CGT : 661,480 13,221 (2.00%) 247, ,252 68,920 (10.42%) (37.35%) (50.23%) 442,749 No. : 1-1 (100.00%) CGT : 79,325-79,325 (100.00%) ,556 No. : (58.82%) 0 (0.00%) 7 (41.18%) 20 CGT : 235, ,418 69,374 0 (0.00%) (70.58%) (29.42%) 293,831 No. : CGT : No. : (45.95%) 3 (8.11%) 17 (45.95%) 29 CGT : 1,390, , , ,467 (8.59%) (43.28%) (48.12%) 1,014,272 No. : (29.55%) 2 (4.55%) 29 (65.91%) 32 CGT : 527, , ,172 41,998 (7.96%) (34.40%) (57.64%) 359,676 No. : 31 1 (3.23%) 12 (38.71%) 5 (16.13%) 13 (41.94%) 21 CGT : 600,668 24,228 (4.03%) 273, ,435 79,443 (13.23%) (45.54%) (37.20%) 457,492 No. : 18-6 (33.33%) 2 (11.11%) 10 (55.56%) 9 CGT : 318, , ,473 29,434 (9.25%) (38.09%) (52.66%) 157,146 No. : 15-5 (33.33%) 1 (6.67%) 9 (60.00%) 11 CGT : 157,459-91,189 (57.91%) 10,326 (6.56%) 55,944 (35.53%) 198,498 No. : 11-6 (54.55%) 1 (9.09%) 4 (36.36%) 2 CGT : 130,539-90,182 (69.08%) 8,698 (6.66%) 31,659 (24.25%) 20,354 No. : 5-3 (60.00%) 1 (20.00%) 1 (20.00%) 6 CGT : 165,360-98,887 (59.80%) 33,687 (20.37%) 32,786 (19.83%) 198,900 No. : 2-1 (50.00%) 0 (0.00%) 1 (50.00%) - CGT : 23,976-7,739 (32.28%) 0 (0.00%) 16,237 (67.72%) - No. : 1-1 (100.00%) CGT : 136, ,825 (100.00%) ,280 No. : (1.39%) 269 (37.26%) 45 (6.23%) 398 (55.12%) 498 CGT: 14,363, ,363 5,844,847 7,436, ,962 (6.57%) (0.96%) (40.69%) (51.77%) 10,407,554 Page 12 of 21

13 Slippage/Advancement in Q2- Segment Bulkers Containers Semi-liner Tonnage LNG (Gas I) LPG (Gas III) Combination Carriers Crude Tanker Product Tanker Product/Chemical Tanker Chemical Tanker Specialised Tanker Specialised Cargo (Specialised Cargo I) Vehicles Carrier (Specialised Cargo II) Heavy-Lift Cargo (Specialised Cargo III) Passenger Ships Total Unit Scheduled Delivery (as per 1 st January) (a) Ahead of Schedule (b) On-time (c) Realised Confirmed deductions / fictitious (d) Slippage (e) Actual Deliveries No. : (6.55%) 65 (23.64%) 22 (8.00%) 170 (61.82%) 182 CGT : 5,096, ,565 1,198,618 3,166, ,729 (7.14%) (7.21%) (23.52%) (62.13%) 3,460,545 No. : (13.41%) 29 (35.37%) 5 (6.10%) 37 (45.12%) 73 CGT : 2,907, ,569 1,136,424 1,139, ,512 (7.21%) (14.50%) (39.09%) (39.20%) 2,655,270 No. : 44 3 (6.82%) 8 (18.18%) 4 (9.09%) 29 (65.91%) 34 CGT : 459,714 44,655 (9.71%) 85,539 (18.61%) 33,792 (7.35%) 295,728 (64.33%) 370,553 No. : 3 1 (33.33%) 1 (33.33%) 1 (33.33%) - 1 CGT : 249,795 79,325 (31.76%) 79,325 (31.76%) ,325 No. : 6 1 (16.67%) 4 (66.67%) 0 (0.00%) 1 (16.67%) 8 CGT : 106,908 18,992 11,196 76,720 (71.76%) 0 (0.00%) (17.76%) (10.47%) 140,562 No. : (0.00%) 3 (100.00%) - CGT : 15, (0.00%) 15,084 (100.00%) - No. : 31 2 (6.45%) 7 (22.58%) 7 (22.58%) 15 (48.39%) 16 CGT : 1,093,099 54,643 (5.00%) 249, , ,365 (25.92%) (22.84%) (46.24%) 617,061 No. : 45 2 (4.44%) 17 (37.78%) 2 (4.44%) 24 (53.33%) 32 CGT : 432,748 33,263 (7.69%) 185, ,717 27,647 (6.39%) (42.78%) (43.15%) 302,328 No. : 13-3 (23.08%) 1 (7.69%) 9 (69.23%) 10 CGT : 277,068-71,712 (25.88%) 14,100 (5.09%) 191,256 (69.03%) 209,434 No. : 9-3 (33.33%) 1 (11.11%) 5 (55.56%) 11 CGT : 188,767-79,167 (41.94%) 14,717 (7.80%) 94,883 (50.26%) 182,179 No. : 11 1 (9.09%) 3 (27.27%) 1 (9.09%) 6 (54.55%) 6 CGT : 202,108 30,135 72,381 89,266 (44.17%) 10,326 (5.11%) (14.91%) (35.81%) 136,132 No. : 4-2 (50.00%) 0 (0.00%) 2 (50.00%) - CGT : 60,837-40,085 (65.89%) 0 (0.00%) 20,752 (34.11%) - No. : 7 2 (28.57%) 3 (42.86%) 1 (14.29%) 1 (14.29%) 3 CGT : 226,466 67,219 33,174 99,373 (43.88%) 26,700 (11.79%) (29.68%) (14.65%) 99,373 No. : 3-2 (66.67%) 0 (0.00%) 1 (33.33%) - CGT : 26,690-15,382 (57.63%) 0 (0.00%) 11,308 (42.37%) - No. : 5 1 (20.00%) 3 (60.00%) 1 (20.00%) - 3 CGT : 532,880 87, ,379 (16.41%) (64.06%) ,379 No. : (7.76%) 150 (27.73%) 46 (8.50%) 303 (56.01%) 379 CGT: 11,875,424 1,204,821 3,747,771 1,179,079 5,743,753 (10.15%) (31.56%) (9.93%) (48.37%) 8,594,141 Page 13 of 21

14 Segment Bulkers Containers Semi-liner Tonnage LNG (Gas I) LPG (Gas III) Combination Carriers Crude Tanker Product Tanker Product/Chemical Tanker Chemical Tanker Specialised Tanker Specialised Cargo (Specialised Cargo I) Vehicles Carrier (Specialised Cargo II) Heavy-Lift Cargo (Specialised Cargo III) Passenger Ships Total Unit Scheduled Delivery (as per 1 st January) (a) Slippage/Advancement in Q3- Ahead of Schedule (b) Page 14 of 21 On-time (c) Realised Confirmed deductions / fictitious (d) Slippage (e) Actual Deliveries No. : (5.73%) 37 (19.27%) 17 (8.85%) 127 (66.15%) 144 CGT : 3,563, , ,306 2,356, ,684 (7.46%) (5.98%) (20.44%) (66.12%) 2,759,509 No. : (19.44%) 20 (27.78%) 8 (11.11%) 30 (41.67%) 47 CGT : 2,656, , ,865 1,001, ,584 (9.40%) (22.38%) (30.53%) (37.69%) 1,765,864 No. : 23 2 (8.70%) 5 (21.74%) 1 (4.35%) 15 (65.22%) 24 CGT : 258,178 30, ,029 50,271 (19.47%) 5,454 (2.11%) (11.78%) (66.63%) 307,324 No. : 6-5 (83.33%) 0 (0.00%) 1 (16.67%) 6 CGT : 508, ,853 82,514 0 (0.00%) (83.77%) (16.23%) 506,362 No. : 7 1 (14.29%) 3 (42.86%) 0 (0.00%) 3 (42.86%) 5 CGT : 125,882 28,904 41,338 55,640 (44.20%) 0 (0.00%) (22.96%) (32.84%) 82,699 No. : CGT : ,793 No. : 19 3 (15.79%) 5 (26.32%) 3 (15.79%) 8 (42.11%) 9 CGT : 700,569 99, , , ,650 (17.51%) (14.18%) (27.10%) (41.21%) 336,367 No. : 19-7 (36.84%) 2 (10.53%) 10 (52.63%) 19 CGT : 262,161-95,608 (36.47%) 26,533 (10.12%) 140,020 (53.41%) 219,660 No. : 11 1 (9.09%) 1 (9.09%) 0 (0.00%) 9 (81.82%) 12 CGT : 265,303 24,400 (9.20%) 24,334 (9.17%) 0 (0.00%) 216,569 (81.63%) 252,672 No. : 11 1 (9.09%) 4 (36.36%) 2 (18.18%) 4 (36.36%) 11 CGT : 207,897 7,245 (3.48%) 97,052 (46.68%) 37,234 (17.91%) 66,366 (31.92%) 234,020 No. : 6 1 (16.67%) 1 (16.67%) 1 (16.67%) 3 (50.00%) 6 CGT : 99,920 29,386 30,104 30,104 (30.13%) 10,326 (10.33%) (29.41%) (30.13%) 88,473 No. : 4 1 (25.00%) 1 (25.00%) 0 (0.00%) 2 (50.00%) - CGT : 41,718 5,072 (12.16%) 18,236 (43.71%) 0 (0.00%) 18,410 (44.13%) - No. : 8-2 (25.00%) 3 (37.50%) 3 (37.50%) 4 CGT : 250,558-65,695 (26.22%) 94,074 (37.55%) 90,789 (36.23%) 134,894 No. : 1 1 (100.00%) CGT : 7,691 7,691 (100.00%) No. : CGT : No. : (9.50%) 91 (24.01%) 37 (9.76%) 215 (56.73%) 288 CGT: 8,947,596 1,040,239 2,591,830 4,503, ,539 (9.07%) (11.63%) (28.97%) (50.34%) 6,704,637 Notes: (1) Slippage / Advancement can be measured in two ways: a) Actual delivery against original contractual delivery. b) Actual delivery against revised contractual delivery (after rescheduling).

15 The figure shown here is combination of both. (2) The basis of the comparison is always the known orderbook 1 st January (of current and preceding year), as unless the base is constant, we are not comparing apple to apple. That means our calculation excludes: a) Spillovers delayed deliveries from the earlier period. For instance, if a vessel is scheduled to be delivered in 1 st Quarter of (2009), but gets delivered in the 3 rd Quarter of (2009), she will not be counted as actual deliveries in 3 rd Q (2009), for the purpose of the slippage calculation. b) Newly surfaced existing orders entered into the system after 1st January of the current and preceding year. For instance, if there were 400 capesize bulkers known at 1st January 2008, the system would just track slippage of these vessels and disregard the 50 "new" orders that could have been entered into the system during 2008, since we can't calculate the extent of slippage by comparing the schedule of 400 ships against delivery of 450 ships. Since spillovers and newly surfaced existing orders are frequent events, the results shown here are slippage of the known orderbook 1st January each year, not necessarily results of the entire orderbook at any given time, however they give very close indications to the extent of slippage. (3) Actual deliveries (f) are mainly from the recorded orderbook 1st January, however it also includes spillovers from earlier periods, additional deliveries from newly surfaced existing orders, and deliveries ahead of schedule from the period (for instance, some orders were scheduled to be delivered in January 2008 however it was delivered in December 2009, hence, this will be included in Actual Deliveries in 2009).In other words, whilst (a) = (b)+(c)+(d)+(e) = 100%, (f) can be smaller (if more ships were delivered in the preceding year/previous quarter) or bigger (from spillover and unknown orders) than (b)+(c). Total deductions (d) = fictitious orders + failed contracts + cancelled and removed + terminated and removed. (4) Slippage = builder/construction delay + rescheduling. a) Quarterly slippage refers to the number of ships or orders that slipped from the quarter to a following quarter. b) Annual slippage refers to the number of ships or orders that slipped from 2010 into Slippage refers to the number of ships and capacity of orders that slipped from the quarter to a following quarter. Page 15 of 21

, Product Tankers (WY Segment 9), Product/Chemical Tankers (WY Segment 10), Chemical Tankers (WY Segment 11), Specialised")

16 Demolitions as verified 25 November Notes: 1. YTD Figures as of 25 November 2. Total Fleet: Total fleet at the end of each year. 3. Tankers include Crude Tankers (WY Segment 8), Product Tankers (WY Segment 9), Product/Chemical Tankers (WY Segment 10), Chemical Tankers (WY Segment 11), Specialised Tankers (WY Segment 12). Page 16 of 21

17 Rescheduling (Delay + Postponement by Mutual Agreement) as verified 25 November Notes: 1. This table only accounts for what is currently on order. Deliveries are excluded months prior to date are deliveries originally scheduled to take place in 12 months prior to date the current date in other words these are delays. 3. Orderbook for the corresponding period/year is the orderbook scheduled to be delivered for a particular year, as per 21 Nov Amount of tonnage Rescheduled (%) = Amount of tonnage Rescheduled over Orderbook for the corresponding period/year. 5. Delay is usually caused by the builder, excessive delay could result in cancellation. 6. Postponement by mutual agreement is part of contractual revision. 7. Tankers include Crude Tankers (WY Segment 8), Product Tankers (WY Segment 9), Product/Chemical Tankers (WY Segment 10), Chemical Tankers (WY Segment 11), Specialised Tankers (WY Segment 12). Page 17 of 21

18 Shipbuilder Developments 28-Oct- : STX Arctech Helsinki Shipyard moving to sale to USC Russia : The Russian state-owned shipbuilding firm USC has confirmed it will take full ownership of the financially challenged Arctech Helsinki shipyard from its current owner, the Korean company STX, according to the Finnish newspaper Yle. United Shipbuilding Corporation (USC) already holds a 50 percent stake in Arctech, and will now take full control when it buys out STX, says Yle, referring to a report in the Russian newspaper Kommersant. Citing USC's head of communications, Aleksei Kravchenko, Yle reports that the timetable is not yet confirmed, but Kravchenko believes the deal could take some time, and the purchase price is under 20 million euros. 13-Oct- : Taizhou Sanfu delivers two bulk carriers to Fujian Highton : On 13 October, Taizhou Sanfu Ship Engineering Co., Ltd. delivers two 51,000 dwt bulkers (SF100116/SF100117) to Fujian Highton Shipping Co., Ltd. The ship is m long, m wide and 16.5 m deep, with designed draft of 10.5 m and structural draft of 10.8 m. Designed speed is 12 knots. CCS is the class. 10-Oct- : Jinling Shipyard launches first 5,000 TEU containership for German owner : On 10 October, Jinling Shipyard launched the first 5,000 TEU containership for its German owner. The ship is m long, 37.3 m wide and 19.6 m deep, primarly used to carry containers and hazardous goods. It is the largest containership that Jinling Shipyard has ever built. The German owner has ordered two such vessels from the yard. 09-Oct- : Hudong Zhonghua starts keel laying for No.3 LNG carrier for ExxonMobil/MOL : On 9 October, Hudong Zhonghua Shipbuilding (Group) Co., Ltd. started keel laying for the third 172,000 CBM LNG carrier for ExxsonMobil/MOL in the dock. On 30 September, the builder launched the second vessel of the series. Named "Southern Cross", the second vessel started keel laying on 14 May. The ship is 290 m long, m wide, m deep, with designed draft of 11.5 m and structural draft of 12.5 m. 08-Oct- : GSI to acquire CSSC Guangzhou Longxue Shipbuilding : Guangzhou Shipyard International has recently announced the plan to issue H stocks to raise fund for acquiring 100% stakes of CSSC Guangzhou Longxue Shipbuilding Co., Ltd. The shares will be placed to CSSC (Hong Kong) Shipping Leasing Ltd., a fully owned subsidiary of CSSC, and Baosteel Resources (International), a fully owned subsidiary of Baosteel Group, and China Shipping (Hong Kong) which is fully owned by China Shipping Group. HKD 2.825bn is expected to be raised, with RMB958m to be used for purchasing 100% stakes from the three mentioned parties. 07-Oct- : Hyundai Samho Heavy Industries launches world's first LNG carrier built onground : Hyundai Samho Heavy Industries (HSHI), a shipbuilding affiliate of Hyundai Heavy Industries, announced today it successfully launched a 162,000 CBM LNG carrier built using the on-ground shipbuilding method for the first time in the world. The vessel, designed for delivering chilled natural gas, was ordered by Golar of Norway in February It is 289 m long, 45.6 m wide and 26 m deep. It is expected to be delivered in late July 2014 after outfitting and painting work. After about 270 large blocks, LNG containment system, an engine, a propeller are manufactured and assembled in the on-land shipbuilding area equipped with a 1,200t gantry crane, four jib cranes and a floating dock, the assembled LNG carrier is loaded out onto a floating dock by hydaulic skidding, then the LNG ship is launched out by submerging the floating dock. LNG carrier is about 30% heavier than other type of ships, one the hydraulic skidding facility and on the floating dock is the critical point of launching. Though this is the first LNG carrier Hyundai Samho has built using the on-ground method, the company has already built 50 other ships using this method since May Page 18 of 21

19 2008. The yard plans to build LNG carriers in its orderbook using the on-ground shipbuilding method which allows higher productivity, cost effectiveness, efficient utilization of facilities and resources, and improvement of safety and working conditions. 01-Oct- : DSME extends Daehan management : Daehan Shipbuilding of Korea released a regulatory filing on August 30 that a contract period for management by Daewoo Shipbuilding & Marine Engineering had been extended by two years and six months from the previous one, June 21, 2011-June 30, 2014, to June 21, 2011-December 31,. The management period was prolonged on conditions of a new financial support, the second passed bill of the 20th Creditor Banks Standing Council and so on. The other parties of this changed contract are Daewoo and Korea Development Bank (main creditor bank of Creditor Banks Standing Council).The board of directors resolution was made on August 28 and the contract extension had been approved by Daewoo s board on August 26. Technology Developments 09-Oct- : Wartsila releases another ECA compliant dual-fuel engine to the US market : Wartsila has now released its Wartsila 20DF dual-fuel engine for sale in the US market. The engine meets the strict emissions compliance criteria of the US Environmental Protect Agency (EPA) Tier 4 and is now available to American ship owners and operators. The Wartsila 20DF is a proven and successful engine and its release to the US market is in response to the growing demand for natural gas fueled engines. The Wartsila 20DF is a commercial duty, medium-speed, dual-fuel engine. Engines supplied to the US amrket will operate primarly on natural gas, with marine diesel oil as a pilot fuel or as an emergency backup fuel. The Wartisla dual-fuel (DF) technology is attracting the attention of global fleet owners operating within the North American Emission Control Area (ECA), for which the regulations came into force in August The legislation is aimed at achieving stricter control on emission of SOx, NOx and particulate matter from vessels. ECA has also been established in the Baltic Sea and the North Sea. 07-Oct- : Rolls-Royce powers world's first gas-powered tug : Rolls-Royce has seen the completion of the world's first gas powered tug in Sanmar Shipyard for Norwegian customer Bukser og Berging. The tug features two Rolls-Royce Bergen C26:33L6PG engines fuelled purely by LNG. The boat, named "Borgoy", will enter service next month following a series of sea trials. It will be operated by Norwegian state oil company Statoil at its Karsto gas terminal. The Rolls-Royce propulsion package includes the gas tank and supply system and two of its latest design US35 azimuth thrusters that ensure the tug has rapid maneuvering and positioning capabilities which are essentials for tug operation. The tug's CO2 emissions will be around 30% lower than conventionally fuelled tugs. Page 19 of 21

20 Others 20-Oct- : Cosco Shipyard to convert QE2 into luxury hotel : The QE2's makeover is scheduled for completion by The Dubai-based owner of the iconic QE2 cruise liner has announced the appointment of COSCO Shipyard Group to refurbish the ship into a luxury floating hotel. QE2 Holdings said in a statement that the cruise ship, which has hosted kings, queens, presidents, prime ministers and celebrities throughout its legendary 40-year history, will depart from Dubai and arrive in COSCO Shipyard s facility in Zhoushan, Zhejiang Province. Once there, it will receive a makeover that is scheduled for completion by The existing 990 staterooms will be converted into 400 premium suites ranging from 60 to 150 square metres. The statement said COSCO Shipyard will be responsible for all the technical repairs and coordinate with an appointed interior renovation contractor to revamp the accommodation and ballroom, as well as the refitting of seven restaurants, 10 lounges, a cinema, a maritime museum displaying QE2 memorabilia, and a shopping mall. Daniel Chui, president and chief executive of QE2 Holdings and managing director of Oceanic Group, said: "The ship's redevelopment is a once-in-a-lifetime opportunity for any interior design professional to create what will become one of Asia s major waterfront tourist attractions.the goal for the final design is to preserve the soul of the QE2 - many of the original furnishings and much of the decor will be incorporated - while creating a modern luxury hotel." Originally set to be refurbished as the central attraction in a maritime-themed development on Palm Jumeirah, this plan was scrapped in the wake of the financial crisis and the downturn in the Dubai property market. 15-Oct- : DNV GL recommends ways to make LNG bunkering safe and efficient : DNV GL has launched a "Recommended Practice for Authorities," LNG bunker suppliers and ship operators which provides guidance on how LNG bunkering can be undertaken in a safe and efficient manner. LNG-fuelled ships have logged over 130 ship-years of operation in Norwegian waters and LNG's attractiveness and stability as a fuel has been thoroughly demonstrated. Globally too, operators, suppliers and regulators have gained significant experience in all aspects of LNG-fuelled ship operations in recent years. However, the process for developing the required infrastructure has not yet been standardised. According to DNV GL, 83 LNG-fuelled ships are in operation or on order worldwide, ranging from passenger ferries, Coast Guard ships and cargo vessels to tankers and platform supply vessels. Estimates say the global LNG-fuelled fleet is to reach 3,200 by EU along is to invest in helping to equip 139 seaports and inland ports with LNG bunker stations by DNV GL is now opening the Recommended Practice for comments for an external six-week consultation period. Subsequently, DNV will update the document based on input received from the industry, followed by formal publication. 10-Oct- : BV to class largest container ships built in China : Bureau Veritas will class three Ultra-Large Container Ships (ULCSs) to be built for China State Shipbuilding Corporation (CSSC) and chartered to French operator CMA CGM. The ships are due for delivery in The 16,000 teu vessels will be the largest container ships built in China to date. One will be built at the Shanghai Waigaoqiao Shipbuilding (SWS) yard, and the other two at Shanghai Jiangnan Changxing Heavy Industry, part of which came under the management of SWS this year. The design was developed by the Marine Design and Research Institute of China (MARIC) in co-operation with BV, which performed the drawing approval and conducted a thorough structural examination. The vessels will have an overall length of 399 m, a beam of 54 m, and a draft of 16 m. Special consideration has been given to hydroelastic design (whipping and springing) issues, which are so important for this size of ship. A hydroelastic examination was performed using BV's HOMER software in order to take into account extreme whipping loads due to slamming and additional fatigue damage due to springing, factoring in the elastic structural Page 20 of 21

21 response of the ship. This review provides a higher level of safety compared to the rigid approach traditionally adopted to such issues, and is mandatory under BV Rules for ULCSs of 300 m and above. On the strength of this examination, BV s WhiSp2 notation has been assigned to the ships. The vessels will be also granted BV s VeriSTAR HULL DFL 25-year notation, which certifies various structural details, including hatch corners and coamings, for 25 years of fatigue life, following a spectral fatigue analysis with a 3D finite element analysis model. The 16,000 teu ships will be able to operate at a maximum speed of over 23 knots with a single-screw propeller directly coupled to a 69 Megawatt, 2-stroke electronic engine. The vessels environmentally friendly profile is attested to by BV s class notations CLEANSHIP and FORS. The latter incorporates special arrangements to ensure that the ship s fuel oil tanks are safely emptied in case of emergency, minimizing the risk of pollution. This is an important safety aspect considering the size of the fuel oil tanks of ULCSs. Steel cutting for the new vessels is due to begin next year and the ships are expected to be delivered in Oct- : MAN signs propeller agreement with DSIC : MAN Diesel & Turbo signed an agreement on 30 August in Denmark regarding the production of its Kappel propeller portfolio with Dalian Marine Propeller Co., Ltd. (DMMP) affiliated to China Shipbuilding Industry Corporation (CSIC). The deal allows DMMP to produce and sell MAN Alpha Kappel design propellers in China. MAN Disel & Turbo subsequently announced that DMMP has signed a Kappel design propeller contract with Xiamen Shipbuilding Industry Co., Ltd. for three + 8,500 CEU PCTC car carriers. The shipowner is Hoegh Autoliners. MAN's facility in Frederikshavn reprots that tank tests on different propeller configurations displayed the Kappel design's superior efficiency compared to other propellers. Worldyards Newsletter is available freely to our subscribers, or can otherwise be ordered as a stand-alone subscription. For details of newsletter subscription please contact us at wy@worldyards.com. Reprinting or reproduction of this newsletter without explicit consent of Worldyards.com Pte Ltd is prohibited. Worldyards reserves the right to publish this newsletter on a complimentary basis 2 months after the month of issue. * Copyright Worldyards.com Pte Ltd, details without guarantee. * At the time of publishing, some orders are still being verified. Please log onto for the most up-todate information. Page 21 of 21

ORDERBOOK OBSERVER M A R C H

ORDERBOOK OBSERVER M A R C H 2 1 7 Tanker Orderbook by Builder Country Rank Country No. Mn Dwt Mn CGT Tanker Orders by Size Segment Share (%) of Total 1 South Korea 18 25.5 5. 38.8% 2 China 159 21.1 4.3

ORDERBOOK OBSERVER M A R C H 2 1 7 Tanker Orderbook by Builder Country Rank Country No. Mn Dwt Mn CGT Tanker Orders by Size Segment Share (%) of Total 1 South Korea 18 25.5 5. 38.8% 2 China 159 21.1 4.3

Korean Shipbuilding Industry & Policy

Korean Shipbuilding Industry & Policy June 6th 2018 MOTIE Ministry of Trade, Industry and Energy Outline 1. Shipbuilding Market (1) 2016 was a year with a historically low level of new-building demand

Korean Shipbuilding Industry & Policy June 6th 2018 MOTIE Ministry of Trade, Industry and Energy Outline 1. Shipbuilding Market (1) 2016 was a year with a historically low level of new-building demand

December 22nd, 2017 / Week 51 THE VIEW FROM THE BRIDGE. Full report can be viewed on the Market Reports tab at the following link:

December 22nd, 2017 / Week 51 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com Highlight of the week was the announced acquisition

December 22nd, 2017 / Week 51 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com Highlight of the week was the announced acquisition

December 15th, 2017 / Week 50 THE VIEW FROM THE BRIDGE. Full report can be viewed on the Market Reports tab at the following link:

December 15th, 2017 / Week 50 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com The BCI index moved slightly lower at the end of the

December 15th, 2017 / Week 50 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com The BCI index moved slightly lower at the end of the

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) August 24th, 2018 / Week 34

August 24th, 2018 / Week 34") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 August 24th, 2018 / Week 34 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 August 24th, 2018 / Week 34 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) February 8th 2019 / Week 6

February 8th 2019 / Week 6") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 February 8th 2019 / Week 6 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 February 8th 2019 / Week 6 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Propulsion of 30,000 dwt. Handysize Bulk Carrier

Propulsion of 3, dwt Handysize Bulk Carrier Content Introduction...5 EEDI and Major Ship and Main Engine Parameters...6 Energy Efficiency Design Index (EEDI)...6 Major propeller and engine parameters...7

Propulsion of 3, dwt Handysize Bulk Carrier Content Introduction...5 EEDI and Major Ship and Main Engine Parameters...6 Energy Efficiency Design Index (EEDI)...6 Major propeller and engine parameters...7

Putting the Right Foot Forward: Strategies for Reducing Costs and Carbon Footprints

Putting the Right Foot Forward: Strategies for Reducing Costs and Carbon Footprints More than 140 years in business Business Segments: Maritime Classification, Maritime Solutions, Oil & Gas and Renewables

Putting the Right Foot Forward: Strategies for Reducing Costs and Carbon Footprints More than 140 years in business Business Segments: Maritime Classification, Maritime Solutions, Oil & Gas and Renewables

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) December 7th 2018 / Week 49

December 7th 2018 / Week 49") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 December 7th 2018 / Week 49 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 December 7th 2018 / Week 49 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

International Economic Outlook Impact on Global Shipping. International Propeller Club Convention Tampa, FL

International Economic Outlook Impact on Global Shipping International Propeller Club Convention Tampa, FL Captain John W. Murray October 7, 2010 Hapag-Lloyd The Company Headquarters in Hamburg, Germany

International Economic Outlook Impact on Global Shipping International Propeller Club Convention Tampa, FL Captain John W. Murray October 7, 2010 Hapag-Lloyd The Company Headquarters in Hamburg, Germany

Unlawful distribution of this report is prohibited. IFCHOR Group Research

Unlawful distribution of this report is prohibited IFCHOR Group Research Marine Money Geneva Forum - 29 th June 2016 DRY BULK SUPPLY OVERVIEW Capacity Surplus... Yearly net fleet change..... FUNDAMENTALS

Unlawful distribution of this report is prohibited IFCHOR Group Research Marine Money Geneva Forum - 29 th June 2016 DRY BULK SUPPLY OVERVIEW Capacity Surplus... Yearly net fleet change..... FUNDAMENTALS

Martin Stopford President, Clarkson Research

9//5 Current and past policies for expanding maintaining or reducing shipbuilding capacity: OECD Working Party No 6 9 th November 5 Martin Stopford President, Clarkson Research Martin Stopford, Clarkson

9//5 Current and past policies for expanding maintaining or reducing shipbuilding capacity: OECD Working Party No 6 9 th November 5 Martin Stopford President, Clarkson Research Martin Stopford, Clarkson

- Shipbuilding Division - Offshore & Engineering and Industrial Plant Division - Engine & Machinery Division

- Shipbuilding Division - Offshore & Engineering and Industrial Plant Division - Engine & Machinery Division - Financial Summary of HHI - Financial Summary of HMD - 2018 New Order HMD 3.9 KCC 6.8 National

- Shipbuilding Division - Offshore & Engineering and Industrial Plant Division - Engine & Machinery Division - Financial Summary of HHI - Financial Summary of HMD - 2018 New Order HMD 3.9 KCC 6.8 National

Propulsion of 46,000-50,000 dwt. Handymax Tanker

Propulsion of 46,-, dwt Handymax Tanker Content Introduction... EEDI and Major Ship and Main Engine Parameters...6 Energy Efficiency Design Index (EEDI)...6 Major propeller and engine parameters...7 46,-,

Propulsion of 46,-, dwt Handymax Tanker Content Introduction... EEDI and Major Ship and Main Engine Parameters...6 Energy Efficiency Design Index (EEDI)...6 Major propeller and engine parameters...7 46,-,

ME-GI/ME-LGI Applications and references

Japanese Yard s Seminar Copenhagen September, 2016 ME-GI/ME-LGI Applications and references René Sejer Laursen Promotion Manager, ME-GI E-mail: ReneS.Laursen@man.eu < 1 > Dual fuel concepts ME-GI vs. ME-LGI

Japanese Yard s Seminar Copenhagen September, 2016 ME-GI/ME-LGI Applications and references René Sejer Laursen Promotion Manager, ME-GI E-mail: ReneS.Laursen@man.eu < 1 > Dual fuel concepts ME-GI vs. ME-LGI

- Shipbuilding Division - Offshore & Engineering and Industrial Plant Division - Engine & Machinery Division

- Shipbuilding Division - Offshore & Engineering and Industrial Plant Division - Engine & Machinery Division - Financial Summary of HHI - Financial Summary of HMD - 2018 New Order & Sales Target HMD 3.9

- Shipbuilding Division - Offshore & Engineering and Industrial Plant Division - Engine & Machinery Division - Financial Summary of HHI - Financial Summary of HMD - 2018 New Order & Sales Target HMD 3.9

The world 1 st LNG-fuelled containership

제품전략 The world 1 st LNG-fuelled containership Focusing on DSME FGSS Technology: HiVAR 27 NOV 2014 Contents 1 Introduction 2 HiVAR System Development 3 Reference Project Status 4 Conclusion 2 The World

제품전략 The world 1 st LNG-fuelled containership Focusing on DSME FGSS Technology: HiVAR 27 NOV 2014 Contents 1 Introduction 2 HiVAR System Development 3 Reference Project Status 4 Conclusion 2 The World

Marine Money Japan Ship Finance Forum

Marine Money Japan Ship Finance Forum Current Situation in Shipbuilding -World and Japan- Masashi Terakado The Shipbuilders Association of Japan May 12th, 2016 Contents 1. Current Situation and Projection

Marine Money Japan Ship Finance Forum Current Situation in Shipbuilding -World and Japan- Masashi Terakado The Shipbuilders Association of Japan May 12th, 2016 Contents 1. Current Situation and Projection

Capital Link's 4th Annual Invest in International Shipping Forum. Dr Hermann J. Klein, Member of Executive Board of GL

Capital Link's 4th Annual Invest in International Shipping Forum The Added Value of Classification to Financial Institutions & Owners in Today's Capital Markets Dr Hermann J. Klein, Member of Executive

Capital Link's 4th Annual Invest in International Shipping Forum The Added Value of Classification to Financial Institutions & Owners in Today's Capital Markets Dr Hermann J. Klein, Member of Executive

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) September 7th 2018 / Week 36

September 7th 2018 / Week 36") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 September 7th 2018 / Week 36 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 September 7th 2018 / Week 36 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Marine Money - Odfjell SE. Leveraging an industrial platform to outperform the cycle

Marine Money - Odfjell SE Leveraging an industrial platform to outperform the cycle Odfjell SE - Key facts Established in 1914 Listed on Oslo Stock Exchange since 1986 One of the worlds largest operator

Marine Money - Odfjell SE Leveraging an industrial platform to outperform the cycle Odfjell SE - Key facts Established in 1914 Listed on Oslo Stock Exchange since 1986 One of the worlds largest operator

TRANSPACIFIC CUSTOMER ADVISORY Implementation of New BAF Formula Effective January 01, 2019

December 7, 2018 TRANSPACIFIC CUSTOMER ADVISORY Implementation of New BAF Formula Effective January 01, 2019 Dear Valued Customer, Bunker is one of the important cost components for a container shipping

December 7, 2018 TRANSPACIFIC CUSTOMER ADVISORY Implementation of New BAF Formula Effective January 01, 2019 Dear Valued Customer, Bunker is one of the important cost components for a container shipping

BUSINESS OVERVIEW FEBRUARY

BUSINESS OVERVIEW FEBRUARY 2018 Except for historical information, the statements made in this presentation constitute forward looking statements. These include statements regarding the intent, belief

BUSINESS OVERVIEW FEBRUARY 2018 Except for historical information, the statements made in this presentation constitute forward looking statements. These include statements regarding the intent, belief

World Record Dual-Fuel Engines Ordered by Leading American Shipping Company

World Record Dual-Fuel Engines Ordered by Leading American Shipping Company Copenhagen, 11/11/2013 LNG-capable ME-GI units to power newbuilding container ships Matson Navigation Company, Inc. a subsidiary

World Record Dual-Fuel Engines Ordered by Leading American Shipping Company Copenhagen, 11/11/2013 LNG-capable ME-GI units to power newbuilding container ships Matson Navigation Company, Inc. a subsidiary

AIR POLLUTION AND ENERGY EFFICIENCY. Update on the proposal for "A transparent and reliable hull and propeller performance standard"

E MARINE ENVIRONMENT PROTECTION COMMITTEE 64th session Agenda item 4 MEPC 64/INF.23 27 July 2012 ENGLISH ONLY AIR POLLUTION AND ENERGY EFFICIENCY Update on the proposal for "A transparent and reliable

E MARINE ENVIRONMENT PROTECTION COMMITTEE 64th session Agenda item 4 MEPC 64/INF.23 27 July 2012 ENGLISH ONLY AIR POLLUTION AND ENERGY EFFICIENCY Update on the proposal for "A transparent and reliable

Propulsion of 2,200-2,800 teu. Container Vessel

Propulsion of 2,2-2,8 teu Container Vessel Content Introduction...5 EEDI and Major Ship and Main Engine Parameters...6 Energy Efficiency Design Index (EEDI)...6 Major propeller and engine parameters...7

Propulsion of 2,2-2,8 teu Container Vessel Content Introduction...5 EEDI and Major Ship and Main Engine Parameters...6 Energy Efficiency Design Index (EEDI)...6 Major propeller and engine parameters...7

LNG fuel as an alternative to low-sulphur marine gas oil for complying with the new emission rules. September 29 th, 2017 Limassol

LNG fuel as an alternative to low-sulphur marine gas oil for complying with the new emission rules September 29 th, 2017 Limassol THE IMO S 2020 GLOBAL SULFUR CAP IMO sets 1 January 2020 for ships to comply

LNG fuel as an alternative to low-sulphur marine gas oil for complying with the new emission rules September 29 th, 2017 Limassol THE IMO S 2020 GLOBAL SULFUR CAP IMO sets 1 January 2020 for ships to comply

Used Vehicle Supply: Future Outlook and the Impact on Used Vehicle Prices

Used Vehicle Supply: Future Outlook and the Impact on Used Vehicle Prices AT A GLANCE When to expect an increase in used supply Recent trends in new vehicle sales Changes in used supply by vehicle segment

Used Vehicle Supply: Future Outlook and the Impact on Used Vehicle Prices AT A GLANCE When to expect an increase in used supply Recent trends in new vehicle sales Changes in used supply by vehicle segment

P. SUMMARY: The Southeastern Power Administration (SEPA) establishes Rate Schedules JW-

establishes Rate Schedules JW-") This document is scheduled to be published in the Federal Register on 08/29/2016 and available online at http://federalregister.gov/a/2016-20620, and on FDsys.gov 6450-01-P DEPARTMENT OF ENERGY Southeastern

This document is scheduled to be published in the Federal Register on 08/29/2016 and available online at http://federalregister.gov/a/2016-20620, and on FDsys.gov 6450-01-P DEPARTMENT OF ENERGY Southeastern

Marine product guide. Engines and generator sets

Marine product guide Engines and generator sets Marine product guide Engines and generator sets Contents Introduction 2 Rating definitions 4 Fuel consumption method 6 Engine model name explanation 7 Propulsion

Marine product guide Engines and generator sets Marine product guide Engines and generator sets Contents Introduction 2 Rating definitions 4 Fuel consumption method 6 Engine model name explanation 7 Propulsion

AMBER M. KLESGES BOARD SECRETARY. No.\w-Tm

\C. 9! J RECOMMENDATION APPROVED; RESOLUTION NO. 16-7999 AND TEMPORARY ORDER 16-7209 & PERMANENT ORDER 16-7210 ADOPTED; BY THE BOARD OF HARBOR COMMISSIONERS \b 1 September 15, 2016 1A THE PORT OF LOS ANGELES

\C. 9! J RECOMMENDATION APPROVED; RESOLUTION NO. 16-7999 AND TEMPORARY ORDER 16-7209 & PERMANENT ORDER 16-7210 ADOPTED; BY THE BOARD OF HARBOR COMMISSIONERS \b 1 September 15, 2016 1A THE PORT OF LOS ANGELES

FOR IMMEDIATE RELEASE

Article No. 7845 Available on www.roymorgan.com Roy Morgan Unemployment Profile Friday, 18 January 2019 Unemployment in December is 9.7% and under-employment is 8.8% FOR IMMEDIATE RELEASE Australian unemployment

Article No. 7845 Available on www.roymorgan.com Roy Morgan Unemployment Profile Friday, 18 January 2019 Unemployment in December is 9.7% and under-employment is 8.8% FOR IMMEDIATE RELEASE Australian unemployment

Propulsion of VLCC Introduction

Propulsion of VLCC Content Introduction...5 EEDI and Major Ship and Main Engine Parameters...6 Energy efficiency design index (EEDI)...6 Minimum propulsion power...6 Major propeller and engine parameters...7,

Propulsion of VLCC Content Introduction...5 EEDI and Major Ship and Main Engine Parameters...6 Energy efficiency design index (EEDI)...6 Minimum propulsion power...6 Major propeller and engine parameters...7,

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) October 26th 2018 / Week 43

October 26th 2018 / Week 43") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 October 26th 2018 / Week 43 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 October 26th 2018 / Week 43 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Monthly Newbuilding Market Report

Monthly Newbuilding Market Report Issue: April 2016 Overview of Ordering Activity (per vessel type / Top Ranking of Contractors) page 1 Ordering Activity (No. of Units ordered, Dwt, Invested Capital) page

Monthly Newbuilding Market Report Issue: April 2016 Overview of Ordering Activity (per vessel type / Top Ranking of Contractors) page 1 Ordering Activity (No. of Units ordered, Dwt, Invested Capital) page

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE

June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at

GASEOUS FUELS SAFETY ASPECTS

Ship Efficiency Conference by The German Society for Maritime Technology Hamburg, 29 September 2009 GASEOUS FUELS SAFETY ASPECTS Bruno DABOUIS 1. REGULATORY CONTEXT 2. USE OF GAS FUEL ENGINES ON SHIPS

Ship Efficiency Conference by The German Society for Maritime Technology Hamburg, 29 September 2009 GASEOUS FUELS SAFETY ASPECTS Bruno DABOUIS 1. REGULATORY CONTEXT 2. USE OF GAS FUEL ENGINES ON SHIPS

OECD Council Working Party on Shipbuilding (WP6) Green Ship Technology Development, Korea and KR

Green Ship Technology Development, Korea and KR") OECD Council Working Party on Shipbuilding (WP6) Submission by KR Green Ship Technology Development, Korea and KR 7~8 July 2011 Kim, Mann-Eung, PhD, Director, Green & Industrial Technology Center Han,

OECD Council Working Party on Shipbuilding (WP6) Submission by KR Green Ship Technology Development, Korea and KR 7~8 July 2011 Kim, Mann-Eung, PhD, Director, Green & Industrial Technology Center Han,

Marine Division. Peter Leifland Alfa Laval Group

Marine Division Peter Leifland Alfa Laval Group Alfa Slide Laval 2 Marine Division by numbers - Order intake (OI) based on LTM September 30, 2018, Order intake: SEK Bn 16.5 (+39%*) Split by type of orders

Marine Division Peter Leifland Alfa Laval Group Alfa Slide Laval 2 Marine Division by numbers - Order intake (OI) based on LTM September 30, 2018, Order intake: SEK Bn 16.5 (+39%*) Split by type of orders

Energy Efficiency Design Index (EEDI)

") Energy Efficiency Design Index (EEDI) Thomas Kirk Director, Environmental Programs STAR Center, Dania Beach, FL 11 April 2012 SOCP Energy Sustainability Meeting Environmental Landscape for Shipping Energy

Energy Efficiency Design Index (EEDI) Thomas Kirk Director, Environmental Programs STAR Center, Dania Beach, FL 11 April 2012 SOCP Energy Sustainability Meeting Environmental Landscape for Shipping Energy

DRY BULK FREIGHT MARKET OUTLOOK MJUNCTION INDIAN STEEL MARKETS CONFERENCE

DRY BULK FREIGHT MARKET OUTLOOK MJUNCTION INDIAN STEEL MARKETS CONFERENCE JUNE 2018 PRESENTATION STRUCTURE where are we in the dry bulk freight market cycle? current freight rates in perspective fundamental

DRY BULK FREIGHT MARKET OUTLOOK MJUNCTION INDIAN STEEL MARKETS CONFERENCE JUNE 2018 PRESENTATION STRUCTURE where are we in the dry bulk freight market cycle? current freight rates in perspective fundamental

GAZIFÈRE INC. Prime Rate Forecasting Process 2017 Rate Case

Overview A consensus forecast is used to estimate the prime rate charged by commercial banks. As the prime rate is subject to competitive pressures faced by individual lenders and is set on an individual

Overview A consensus forecast is used to estimate the prime rate charged by commercial banks. As the prime rate is subject to competitive pressures faced by individual lenders and is set on an individual

The Norwegian NOx Fund Experiences gained so far. Sveinung Oftedal

The Norwegian NOx Fund Experiences gained so far Sveinung Oftedal NOx tax in Norway from 2007 Fiscal NOx tax Fiscal NOx tax 1 st of January 2007 of 1,9 per kg NOx Engines exceeding 750 kw, boilers over

The Norwegian NOx Fund Experiences gained so far Sveinung Oftedal NOx tax in Norway from 2007 Fiscal NOx tax Fiscal NOx tax 1 st of January 2007 of 1,9 per kg NOx Engines exceeding 750 kw, boilers over

Aegean Marine Petroleum Network Inc.

Aegean Marine Petroleum Network Inc. First Quarter 2007 Conference Call May 24, 2007 Disclosure Today s s presentation and discussion will contain forward-looking statements within the meaning of the Private

Aegean Marine Petroleum Network Inc. First Quarter 2007 Conference Call May 24, 2007 Disclosure Today s s presentation and discussion will contain forward-looking statements within the meaning of the Private

WÄRTSILÄ CORPORATION SEB FINNISH BLUE CHIP SEMINAR 28 AUGUST Marco Wirén, CFO. Wärtsilä

WÄRTSILÄ CORPORATION SEB FINNISH BLUE CHIP SEMINAR 28 AUGUST 2015 Marco Wirén, CFO 1 This is Wärtsilä Energy Solutions, 23% Marine Solutions, 30% Services, 47% 2 Net sales and profitability MEUR 6000 14%

WÄRTSILÄ CORPORATION SEB FINNISH BLUE CHIP SEMINAR 28 AUGUST 2015 Marco Wirén, CFO 1 This is Wärtsilä Energy Solutions, 23% Marine Solutions, 30% Services, 47% 2 Net sales and profitability MEUR 6000 14%

MDT TIER III options with low sulphur fuels

Greener Shipping Summit Athens, Greece, 10.11. 2015 MDT TIER III options with low sulphur fuels Michael Jeppesen Promotion Manager Sales & Customer Support Marine Low Speed < 1 > Agenda Greener Shipping

Greener Shipping Summit Athens, Greece, 10.11. 2015 MDT TIER III options with low sulphur fuels Michael Jeppesen Promotion Manager Sales & Customer Support Marine Low Speed < 1 > Agenda Greener Shipping

Ship Efficiency from the Viewpoint of a Financing Bank

Ship Efficiency from the Viewpoint of a Financing Bank Dr. Carsten Wiebers Bank aus Verantwortung KfW IPEX-Bank Responsible Banking Employment cruise Global Integration European investments European offshore

Ship Efficiency from the Viewpoint of a Financing Bank Dr. Carsten Wiebers Bank aus Verantwortung KfW IPEX-Bank Responsible Banking Employment cruise Global Integration European investments European offshore

Consistent implementation of the 2020 sulphur limit and work to further address GHG emissions from international shipping

Consistent implementation of the 2020 sulphur limit and work to further address GHG emissions from international shipping IBIA/BMS United A glimpse into the future of shipping 30 May 2018, Athens, Greece

Consistent implementation of the 2020 sulphur limit and work to further address GHG emissions from international shipping IBIA/BMS United A glimpse into the future of shipping 30 May 2018, Athens, Greece

KCC 6.8 HMD 3.9. National Pension 9.1. Hyundai Motors 2.9. HHI Holdings Asan Foundation 3.0. Treasury Stock 0.1. Others 46.5

HMD 3.9 KCC 6.8 National Pension 9.1 Hyundai Motors 2.9 HHI Holdings 27.7 Asan Foundation 3.0 Others 46.5 Treasury Stock 0.1 1973 ~ 2010 2011 ~ 2018 12. 1973 Establishment of Hyundai Shipbuilding & Heavy

HMD 3.9 KCC 6.8 National Pension 9.1 Hyundai Motors 2.9 HHI Holdings 27.7 Asan Foundation 3.0 Others 46.5 Treasury Stock 0.1 1973 ~ 2010 2011 ~ 2018 12. 1973 Establishment of Hyundai Shipbuilding & Heavy

LNG: Legal and regulatory framework. Canepa Monica World Maritime University

LNG: Legal and regulatory framework Canepa Monica World Maritime University Source: Verisk Maplecroft AIR QUALITY INDEX 2017 Policies and legal instruments for clean energy to support LNG GLOBAL REGIONAL

LNG: Legal and regulatory framework Canepa Monica World Maritime University Source: Verisk Maplecroft AIR QUALITY INDEX 2017 Policies and legal instruments for clean energy to support LNG GLOBAL REGIONAL

AIR POLLUTION AND ENERGY EFFICIENCY. Mandatory reporting of attained EEDI values. Submitted by Japan, Norway, ICS, BIMCO, CLIA, IPTA and WSC SUMMARY

E MARINE ENVIRONMENT PROTECTION COMMITTEE 73rd session Agenda item 5 MEPC 73/5/5 9 August 2018 Original: ENGLISH AIR POLLUTION AND ENERGY EFFICIENCY Mandatory reporting of attained EEDI values Submitted

E MARINE ENVIRONMENT PROTECTION COMMITTEE 73rd session Agenda item 5 MEPC 73/5/5 9 August 2018 Original: ENGLISH AIR POLLUTION AND ENERGY EFFICIENCY Mandatory reporting of attained EEDI values Submitted

The Challenge for Today s Shipbuilding Companies

Digital Ship Japan 2014 The Challenge for Today s Shipbuilding Companies Sharing Japanese Shipbuilding, Shipping, and Maritime Technologies with the World Sep. 2 2014 Fumihiko Shibata, Deputy General Manager

Digital Ship Japan 2014 The Challenge for Today s Shipbuilding Companies Sharing Japanese Shipbuilding, Shipping, and Maritime Technologies with the World Sep. 2 2014 Fumihiko Shibata, Deputy General Manager

MAN Diesel & Turbo s Solutions for LNG Fuelled Vessels. Christodoulopoulos Dionissis Managing Director Poseidon Med, 8/12/16 Piraeus

MAN Diesel & Turbo s Solutions for LNG Fuelled Vessels Christodoulopoulos Dionissis Managing Director Poseidon Med, 8/12/16 Piraeus < 1 > Agenda 1 Evironmental Regulations 2 Product Portfolio 3 References,

MAN Diesel & Turbo s Solutions for LNG Fuelled Vessels Christodoulopoulos Dionissis Managing Director Poseidon Med, 8/12/16 Piraeus < 1 > Agenda 1 Evironmental Regulations 2 Product Portfolio 3 References,

Newbuildings & Yards 20 June Marine Money Week New York Prepared by Angelica Kemene Head of Market Analysis & Intelligence

Newbuildings & Yards 2 June 218 Marine Money Week New York Prepared by Angelica Kemene Head of Market Analysis & Intelligence Sectors: Cycle Position May 218 % deviation from earnings average 29-218 China

Newbuildings & Yards 2 June 218 Marine Money Week New York Prepared by Angelica Kemene Head of Market Analysis & Intelligence Sectors: Cycle Position May 218 % deviation from earnings average 29-218 China

Emission control at marine terminals

Emission control at marine terminals Results of recent CONCAWE studies BACKGROUND The European Stage 1 Directive 94/63/EC on the control of volatile organic compound (VOC) emissions mandates the installation

Emission control at marine terminals Results of recent CONCAWE studies BACKGROUND The European Stage 1 Directive 94/63/EC on the control of volatile organic compound (VOC) emissions mandates the installation

FOR IMMEDIATE RELEASE

Article No. 6928 Available on www.roymorgan.com Roy Morgan Unemployment Profile Wednesday, 17 August 2016 Australian real unemployment jumps to 10.5% (up 0.9%) in July during post-election uncertainty

Article No. 6928 Available on www.roymorgan.com Roy Morgan Unemployment Profile Wednesday, 17 August 2016 Australian real unemployment jumps to 10.5% (up 0.9%) in July during post-election uncertainty

Recent and current developments in the regulation of air pollution from ships

Recent and current developments in the regulation of air pollution from ships Christiana Ntouni, Regulatory Affairs Working together for a safer world Contents International Maritime Organization (IMO)

Recent and current developments in the regulation of air pollution from ships Christiana Ntouni, Regulatory Affairs Working together for a safer world Contents International Maritime Organization (IMO)

MARITIME GLOBAL SULPHUR CAP. Know the different choices and challenges for on-time compliance SAFER, SMARTER, GREENER

MARITIME GLOBAL SULPHUR CAP 2020 Know the different choices and challenges for on-time compliance SAFER, SMARTER, GREENER Global sulphur cap 2020 DNV GL 3 INTRODUCTION The global 0.5% sulphur cap will

MARITIME GLOBAL SULPHUR CAP 2020 Know the different choices and challenges for on-time compliance SAFER, SMARTER, GREENER Global sulphur cap 2020 DNV GL 3 INTRODUCTION The global 0.5% sulphur cap will

AIR POLLUTION AND ENERGY EFFICIENCY. EEDI reduction beyond phase 2. Submitted by Liberia, ICS, BIMCO, INTERFERRY, INTERTANKO, CLIA and IPTA SUMMARY

E MARINE ENVIRONMENT PROTECTION COMMITTEE 73rd session Agenda item 5 MEPC 73/5/10 17 August 2018 Original: ENGLISH AIR POLLUTION AND ENERGY EFFICIENCY EEDI reduction beyond phase 2 Submitted by Liberia,

E MARINE ENVIRONMENT PROTECTION COMMITTEE 73rd session Agenda item 5 MEPC 73/5/10 17 August 2018 Original: ENGLISH AIR POLLUTION AND ENERGY EFFICIENCY EEDI reduction beyond phase 2 Submitted by Liberia,

PROJECT RESOLUTE. Canadian Coast Guard Icebreaker Support Program Government of Canada solicitation number: F /A

PROJECT RESOLUTE Canadian Coast Guard Icebreaker Support Program Government of Canada solicitation number: F7017-160056/A icebreaker briefing RESOLUTE.indd 1 A unique opportunity at a perfect time in the

PROJECT RESOLUTE Canadian Coast Guard Icebreaker Support Program Government of Canada solicitation number: F7017-160056/A icebreaker briefing RESOLUTE.indd 1 A unique opportunity at a perfect time in the

Monitoring, reporting and verification of CO 2 emissions from ships - EU MRV regulation and obligations and the parallel IMO activities

Monitoring, reporting and verification of CO 2 emissions from ships - EU MRV regulation and obligations and the parallel IMO activities ENAMOR Seminar 22 th November 2016 PIRAEUS HOTEL SAVOY Krzysztof

Monitoring, reporting and verification of CO 2 emissions from ships - EU MRV regulation and obligations and the parallel IMO activities ENAMOR Seminar 22 th November 2016 PIRAEUS HOTEL SAVOY Krzysztof

Pollution by the Shipping Industry: Current Vessels and the Next Generation of Ships

Pollution by the Shipping Industry: Current Vessels and the Next Generation of Ships Presented by Helen Noble 3 April 2014 Pollution by the Shipping Industry Oil pollution Exhaust Gas Emissions Acoustic

Pollution by the Shipping Industry: Current Vessels and the Next Generation of Ships Presented by Helen Noble 3 April 2014 Pollution by the Shipping Industry Oil pollution Exhaust Gas Emissions Acoustic

Electrovaya Provides Business Update

News for Immediate Release Electrovaya Provides Business Update Toronto, Ontario November 8, 2016 Electrovaya Inc. (TSX: EFL) (OTCQX:EFLVF) is providing the following update on business developments previously

News for Immediate Release Electrovaya Provides Business Update Toronto, Ontario November 8, 2016 Electrovaya Inc. (TSX: EFL) (OTCQX:EFLVF) is providing the following update on business developments previously

- 1 - Agenda item 10(e) Emissions from fuel used for international aviation and maritime transport

Emissions from fuel used for international aviation and maritime transport") - 1 - Note by the International Maritime Organization to the thirty-eighth session of the Subsidiary Body for Scientific and Technological Advice (SBSTA 38) Bonn, Germany, 3 to 14 June 2013 Agenda item

- 1 - Note by the International Maritime Organization to the thirty-eighth session of the Subsidiary Body for Scientific and Technological Advice (SBSTA 38) Bonn, Germany, 3 to 14 June 2013 Agenda item

FOR IMMEDIATE RELEASE

Article No. 5842 Available on www.roymorgan.com Roy Morgan Unemployment Profile Thursday, 2 October 2014 Unemployment climbs to 9.9% in September as full-time work lowest since October 2011; 2.2 million

Article No. 5842 Available on www.roymorgan.com Roy Morgan Unemployment Profile Thursday, 2 October 2014 Unemployment climbs to 9.9% in September as full-time work lowest since October 2011; 2.2 million

Opening keynote: Setting the scene the shipowners and shipmanagers point of view

IBIA Annual Convention Hamburg 2014 04 November 2014, Hamburg Dr Hermann J. Klein, CEO E.R. Schiffahrt Opening keynote: Setting the scene the shipowners and shipmanagers point of view Change of shipping

IBIA Annual Convention Hamburg 2014 04 November 2014, Hamburg Dr Hermann J. Klein, CEO E.R. Schiffahrt Opening keynote: Setting the scene the shipowners and shipmanagers point of view Change of shipping

WÄRTSILÄ CORPORATION

WÄRTSILÄ CORPORATION JP MORGAN EUROPEAN CAPITAL GOODS CEO CONFERENCE 13 JUNE 2014 Björn Rosengren, President & CEO 1 Net sales by business 1-3/2014 Ship Power 38% Services 43% Power Plants 19% 2 Net sales

WÄRTSILÄ CORPORATION JP MORGAN EUROPEAN CAPITAL GOODS CEO CONFERENCE 13 JUNE 2014 Björn Rosengren, President & CEO 1 Net sales by business 1-3/2014 Ship Power 38% Services 43% Power Plants 19% 2 Net sales

RESIDENTIAL WASTE HAULING ASSESSMENT SERVICES. January 10, 2011 Presentation to Arvada City Council

RESIDENTIAL WASTE HAULING ASSESSMENT SERVICES January 10, 2011 Presentation to Arvada City Council CONSULTANT TEAM LBA Associates MSW Consultants Denver based recycling and waste management consultant

RESIDENTIAL WASTE HAULING ASSESSMENT SERVICES January 10, 2011 Presentation to Arvada City Council CONSULTANT TEAM LBA Associates MSW Consultants Denver based recycling and waste management consultant

Innovative Power Transmission. Gear Units for LNG Carriers Dual-Fuel/Electric Propulsion

Innovative Power Transmission Gear Units for LNG Carriers Dual-Fuel/Electric Propulsion RENK - Leading Propulsion Technology Customized gear units for LNG carriers Dual-fuel/electric propulsion RENK marine

Innovative Power Transmission Gear Units for LNG Carriers Dual-Fuel/Electric Propulsion RENK - Leading Propulsion Technology Customized gear units for LNG carriers Dual-fuel/electric propulsion RENK marine

Recent Developments in International Seaborne Trade and Maritime Transport

Recent Developments in International Seaborne Trade and Maritime Transport IFSPA, Hong Kong, 3-5 June 2013 Dr. Vincent F. Valentine Officer-in-Charge, Transport Section Division on Technology and Logistics

Recent Developments in International Seaborne Trade and Maritime Transport IFSPA, Hong Kong, 3-5 June 2013 Dr. Vincent F. Valentine Officer-in-Charge, Transport Section Division on Technology and Logistics

FOR IMMEDIATE RELEASE

Article No. 7353 Available on www.roymorgan.com Roy Morgan Unemployment Profile Wednesday, 11 October 2017 2.498 million Australians (18.9%) now unemployed or under-employed In September 1.202 million

Article No. 7353 Available on www.roymorgan.com Roy Morgan Unemployment Profile Wednesday, 11 October 2017 2.498 million Australians (18.9%) now unemployed or under-employed In September 1.202 million

Company Overview. Fleet Profile. Key Facts

STIFEL Conference Presentation February 12, 2019 Company Overview Scorpio Bulkers Inc. ( Scorpio or the Company ) owns or finance leases 56 mid-size dry bulk Eco vessels with an average age of 3.0 years

STIFEL Conference Presentation February 12, 2019 Company Overview Scorpio Bulkers Inc. ( Scorpio or the Company ) owns or finance leases 56 mid-size dry bulk Eco vessels with an average age of 3.0 years

L27/38 GenSets Ordered for TML Heavy Transport Vessels

MAN power for innovative SeaMetric heavy-lifters L27/38 GenSets Ordered for TML Heavy Transport Vessels 11 February 2008. SeaMetric International AS, Stavanger, Norway has during December 2007 ordered

MAN power for innovative SeaMetric heavy-lifters L27/38 GenSets Ordered for TML Heavy Transport Vessels 11 February 2008. SeaMetric International AS, Stavanger, Norway has during December 2007 ordered

BMW Group posts record earnings for 2010

10.03.2011 BMW Group posts record earnings for 2010 Profit before tax rises to euro 4,836 million Profit before financial result climbs to euro 5,094 million Automobiles segment reports EBIT of euro 4,355

10.03.2011 BMW Group posts record earnings for 2010 Profit before tax rises to euro 4,836 million Profit before financial result climbs to euro 5,094 million Automobiles segment reports EBIT of euro 4,355

Future Marine Fuel Quality Changes: How might terminals prepare?

Future Marine Fuel Quality Changes: How might terminals prepare? Further reading from IHS: What Bunker Fuel for the High Seas? A global study on marine bunker fuel and how it can be supplied ABOUT IHS

Future Marine Fuel Quality Changes: How might terminals prepare? Further reading from IHS: What Bunker Fuel for the High Seas? A global study on marine bunker fuel and how it can be supplied ABOUT IHS

Marine & Diesel Division

Marine & Diesel Division Peter Leifland Executive Vice President Alfa Laval Group Industry mix and growth drivers - Distribution of orders LTM September 2015 Ship building Marine Environ., Gas & Energy

Marine & Diesel Division Peter Leifland Executive Vice President Alfa Laval Group Industry mix and growth drivers - Distribution of orders LTM September 2015 Ship building Marine Environ., Gas & Energy

FOR IMMEDIATE RELEASE

Article No. 7433 Available on www.roymorgan.com Roy Morgan Unemployment Profile Friday, 12 January 2018 2.6m Australians unemployed or under-employed in December The latest data for the Roy Morgan employment

Article No. 7433 Available on www.roymorgan.com Roy Morgan Unemployment Profile Friday, 12 January 2018 2.6m Australians unemployed or under-employed in December The latest data for the Roy Morgan employment

3. Steam Turbines and Boilers

3. Steam Turbines and Boilers 3.1. Steam turbines 3.1.1 Steam turbines as a main engine In 2016, Kawasaki Heavy Industries, Ltd. (KHI) delivered a URA Type Marine Propulsion Turbine for an LNG carrier

3. Steam Turbines and Boilers 3.1. Steam turbines 3.1.1 Steam turbines as a main engine In 2016, Kawasaki Heavy Industries, Ltd. (KHI) delivered a URA Type Marine Propulsion Turbine for an LNG carrier