Newbuildings & Yards 20 June Marine Money Week New York Prepared by Angelica Kemene Head of Market Analysis & Intelligence

|

|

|

- Anna Lawson

- 5 years ago

- Views:

Transcription

1 Newbuildings & Yards 2 June 218 Marine Money Week New York Prepared by Angelica Kemene Head of Market Analysis & Intelligence

2 Sectors: Cycle Position May 218 % deviation from earnings average China Newbuilding Price Index Clean Products(MR) Aframax -76.4% % 12 Suezmax % Tanker Markets have turned weak Handysize TC Average VLCC -18.9% 8.47% 1 Supramax TC Average Panamax TC Average -.65% 7.38% 8 Capesize TC Average Bulk carrier & Container rates improve further after the extremely weak 216 Neo-Panamax 9 teu -2.66% 4.55% 6 CNDPI CNTPI CNCPI Containership 44 teu gls % Feeder Containership 17 teu grd 5.44% -15% -1% -5% % 5% 4 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 % change in average earnings from the average Source Data: CNPI

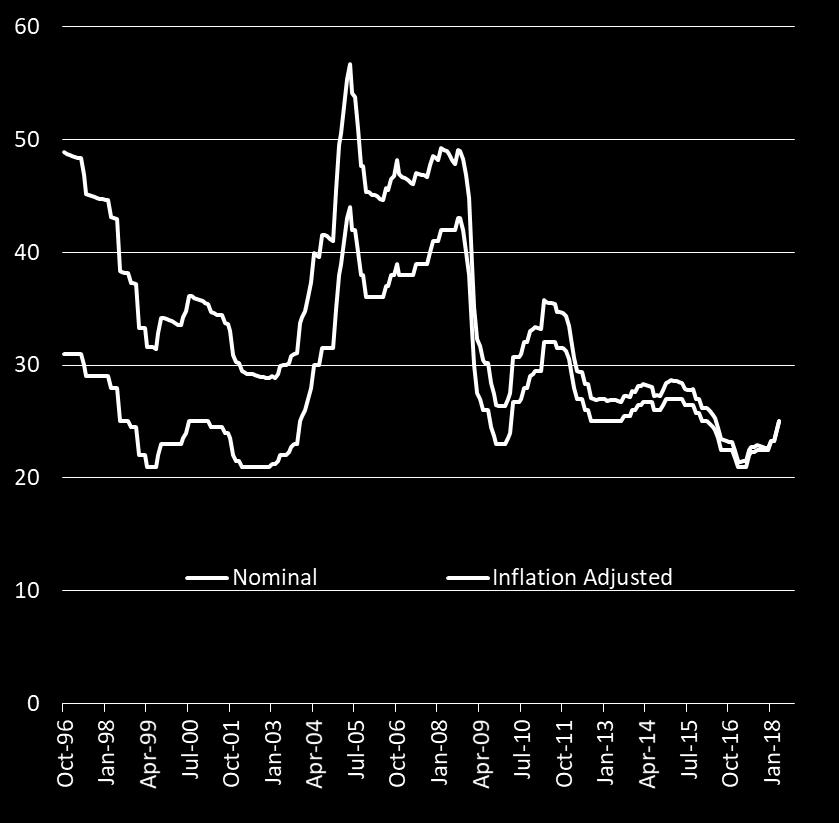

3 Newbuilding Prices out of the bottom - Bulkers 81K DWT Panamax Bulkcarrier NB Prices 61-64K DWT Supramax NB Prices $ Mln 9 6 $ Mln 8 Nominal Inflation adjusted Nominal Inflation adjusted

4 Newbuilding Prices - Tankers Suezmax Tanker K DWT Newbuilding Prices Products Tanker 47-51K DWT Newbuilding Prices 16 $ Mln Suezmax Tanker K DWT Newbuilding Prices 14 inflation adj Suezmax NB price Nominal Inflation adjusted

5 Newbuilding Prices - Containers Containers 17 TEU Newbuilding Prices Containers 88 TEU Newbuilding Prices

6 Base Payment Terms What about options placement? Bulk Carriers Payment Term 1% 1% 1% 1% 6% Key Point Contract Signing Steel Cutting Keel Laying Launching Delivery Months Before Delivery Oil Tankers Payment Term 1% 1% 1% 1% 6% Key Point Contract Signing Steel Cutting Keel Laying Launching Delivery Months Before Delivery Containers Payment Term 1% 1% 1% 1% 6% Key Point Contract Signing Steel Cutting Keel Laying Launching Delivery Months Before Delivery Source Data: Optima Shipping Services, CNPI

7 Yards revenue and deliveries in the 3 major sectors Bulkers, Oil Tankers & Containers: Deliveries vs Yard revenue 8, Million $ Million DWT 16 7, 6, Sum of Deadweight (rhs) $ million , 1 4, 8 3, 6 2, 4 1,

8 A shift towards Chinese Ship Yards Major Shipbuilding Countries Current Orderbook % Products Tanker Crude Oil Tanker Container Bulk Carrier % 2% 4% 6% 8% 1% China, People's Republic Of Korea, South Japan Others For the 3 major sectors there are currently 188 active yards of which 35% is expected to deliver their final order this year, whilst 78% of them will deliver their final order until the end of 219. In yards received more than 1 order, while in yards received more than 1 order A decrease of 68%. Inability to secure orders at a profit. Issue: Yard Consolidation China: Plans on structural reform in shipbuilding industry China s top 1 stateowned shipbuilders will be responsible for 7% of the country s new tonnage by 22. Japan follows the trend (capacity cuts & mergers), but S. Korea remains skeptical. Cost increase: steel prices, labor cost, exchange rates. The extra cost can be balanced if builders charge higher.

9 Asset Play with Newbuildings Older years vs 218 Asset play was always on the table, but times have changed. Market dynamics have altered: financing, new regulations, shorter cycles, AI Need for access to capital, buy fleets instead of a ship, flexibility for financial structuring The asset play in newbuildings is a different game now.

10 Sectors: Fleet Age Profile Bulk Carriers: Existing Fleet Age Profile Tankers: Existing Fleet Age Profile VLCC/ULCC Suezmax/LR Aframax/LR Panamax/LR MR1/MR Handysize % 2% 4% 6% 8% 1% -4 yrs 5-9 yrs 1-14 yrs yrs 2 yrs & over

11 Sectors: Fleet Age Profile Containers: Existing Fleet Age Profile Contracting Pace in major sectors No of Contracts 15, + TEUs ,-14,999 TEUs 8,-11,999 TEUs No expectation to return to firm levels though 6,-7,999 TEUs ,-5,999 TEUs Feeder % 1% 2% 3% 4% 5% 6% 7% 8% 9% 1% -4 yrs 5-9 yrs 1-14 yrs yrs 2 yrs & over Bulk Carrier Containers Crude Oil Tanker Products Tanker

12 Forward Delivery Schedule No of vessels 25 OrderBook as % of the fleet Bulk Carriers OB: 14.5% Capes 8.6% Pmax 5.5% Supras 5.4% Hsize 5 Capesize Panamax BC Supramax Handysize VLCC Suezmax Aframax Panamax Tanker LR2 LR1 MR/Handy Post Panamax Container >15, TEU Bulk Carriers Oil Tankers Containers Neo Panamax k TEU Neo Panamax TEU 3-7.9k TEU Feeder < 3k TEU Oil Tankers OB: 15% VLCCs 8.5% Suezmax 13.2% Afras 9%Pmax 11% LR2 7% LR1 8% MRs/Handies Containers OB: 2.2% >8K TEU 1.14% 3-7.9K TEU 9% Feeders

13 Orderbook Accuracy & Slippage Bulk Carriers Orderbook Containers Orderbook Mll DWT 218 slippage at 2% of 218 orders For the % of the orders have not yet started 1 Mll DWT slippage at 12% of 218 orders For the % of the orders have not yet started Bulkers On Order Building Bulkers On order not yet started Containers On Order Building Containers On order not yet started Source Data: Optima Shipping Services

14 Orderbook Accuracy & Slippage Crude Oil Tankers Orderbook Product Tankers Orderbook 3 Mll DWT 9 Mll DWT Crude Tankers On order not yet started Crude Tankers On Order Building 218 slippage at 27.3% of 218 orders For the % of the orders have not yet started Product Tankers On order not yet started Product Tankers On Order Building 218 slippage at 3% of 218 orders For the % of the orders have not yet started Source Data: Optima Shipping Services

15 Orderbook Replacement Tonnage in Mll DWT SOx Orderbook vs Vessels age above 2 years old Orderbook vs Vessels age above 15 years old Crude Tankers Product Tankers Bulkers Containers Crude Tankers Product Tankers Bulkers Containers age above 2 yrs old Orderbook age above 15 yrs old Orderbook Source Data: Optima Shipping Services

16 Orderbook Replacement Tonnage in Mll DWT SOx Tier 2 Delivery Retrofit like 2 nd hand market Wait and see attitude SOx compliance Scrubber Ready marginally the majority of the orderbook Scrubber Fitted

17 Produced by Optima Shipbrokers Research 1, Ouranou Str Kavouri Vouliagmenis Greece Tel: THANK YOU! This report has been prepared by Optima Shipbrokers and is addressed to Optima Shipbrokers customers only and is for distribution only under such circumstances as may be permitted by applicable law. This information has no regard to specific investment objectives, financial situation or particular needs of any specific recipient. It is published solely for informational purposes and this information is not, and should not be construed as, an offer or solicitation to sell or buy any product, investment, security or any other financial instrument. Optima Shipbrokers does not make any representation or warranty, express or implied, as to the accuracy, completeness or correctness of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the report. Neither Optima Shipbrokers, nor any of its directors, employees or agents, accepts any liability for any loss or damage, howsoever caused, arising from any reliance on any information or views contained in this report. While this report, and any opinions expressed in it, have been derived from sources believed to be reliable and in good faith they are not to be relied upon as authoritative or taken in substitution for the exercise of your own commercial judgment. Any opinions expressed in this report are subject to change without notice. Optima Shipbrokers is under no obligation to update or keep current the information contained herein. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Optima Shipbrokers accepts no liability whatsoever for the action of third parties in the respect. This information is the intellectual property of Optima Shipbrokers. Optima Shipbrokers logo is the trademark of the company. All rights reserved.

18 Up to 3mbd of HSFO bunker demand may be displaced Global Residual Fuel Oil demand by sector Bunker Demand Source Data: Shell International According to SHELL, the transition to.5% Sulphur will cause more changes to global marine industry that the switch to the.1 Sulphur fuel in the ECAs. The impact of this transition represents approximately 75% of global marine fuel demand when compared to the demand of ECA.

19 Who will convert, finally? Alternative fuels are likely to be a more viable option for smaller vessels, while scrubbers are more suitable for larger vessels due to their increased fuel consumption and benefits of economies of scale. Each vessel is different, so specific studies on each should be made. An additional hidden cost is the approximately 2% additional energy needed to run a scrubber. Cheap Fuel Oil in 22 will not guarantee cheap HSFO bunkers: Logistic Margin: maintaining HSFO infrastructure will become a lot more expensive. Inelastic Demand: a number of suppliers have already advised owners and operators looking to use scrubbers in 22 to lock up their volume now so they can ensure future supply. Blended fuels will be considered a very attractive option and may be cheaper than MGO. The price of MDO today might be the best indicator for foreseeing the complying diesel oil price in 22. Some oil majors have indicated that the price for low Sulphur HFO would be somewhere between the current HFO and MDO prices. Naturally, nobody knows what the actual prices at that time will be. Doing nothing is not an option IMO, BIMCO, INTERTANKO, ICS are all united and the flag states are on board for the end results, although the means to get there are not clear. Source Data: Eikon Reuters

20 $/tn $/Day Is there a real impact in vessel earnings? Bunker Prices vs Vessel Earnings TC Rate Pmax TC Rate Afra MDO Spore IFO 38 Spore Limited evidence fuel costs impact vessel earnings However, they do impact voyage costs We would expect some extra 1knot speed (slow steaming) reduction to appear if fuel costs soar to high levels. Expectations are that since the 2H 219 the shipping and the refining market will start seeing changes in fuel demand, supply and prices. Currently, swap curves for middle distillates and fuel oil are in backwardation implying that the IMO22 has not yet invaded into the oil market. But it will soon do! No move yet into longer term supply contracts. 1 Source Data: Shell International 2 Fuel Oil Forward curve, $/tonne Jan- Jan-2 Jan-4 Jan-6 Jan-8 Jan-1 Jan-12 Jan-14 Jan-16 Jan-18 Source Data: Eikon Reuters

Monthly Newbuilding Market Report

Monthly Newbuilding Market Report Issue: April 2016 Overview of Ordering Activity (per vessel type / Top Ranking of Contractors) page 1 Ordering Activity (No. of Units ordered, Dwt, Invested Capital) page

Monthly Newbuilding Market Report Issue: April 2016 Overview of Ordering Activity (per vessel type / Top Ranking of Contractors) page 1 Ordering Activity (No. of Units ordered, Dwt, Invested Capital) page

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE

June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 June 8th, 2018 / Week 23 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) August 24th, 2018 / Week 34

August 24th, 2018 / Week 34") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 August 24th, 2018 / Week 34 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 August 24th, 2018 / Week 34 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Unlawful distribution of this report is prohibited. IFCHOR Group Research

Unlawful distribution of this report is prohibited IFCHOR Group Research Marine Money Geneva Forum - 29 th June 2016 DRY BULK SUPPLY OVERVIEW Capacity Surplus... Yearly net fleet change..... FUNDAMENTALS

Unlawful distribution of this report is prohibited IFCHOR Group Research Marine Money Geneva Forum - 29 th June 2016 DRY BULK SUPPLY OVERVIEW Capacity Surplus... Yearly net fleet change..... FUNDAMENTALS

Regulations : Compliance Challenges and Impact on Dry Bulk Overcapacity

IFCHOR Research Regulations 2017-2020: Compliance Challenges and Impact on Dry Bulk Overcapacity Marine Money - Geneva Forum, June 2017 1 Regulations 2017-2020 Roadmap.... Compliance Challenges Low Sulphur

IFCHOR Research Regulations 2017-2020: Compliance Challenges and Impact on Dry Bulk Overcapacity Marine Money - Geneva Forum, June 2017 1 Regulations 2017-2020 Roadmap.... Compliance Challenges Low Sulphur

December 22nd, 2017 / Week 51 THE VIEW FROM THE BRIDGE. Full report can be viewed on the Market Reports tab at the following link:

December 22nd, 2017 / Week 51 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com Highlight of the week was the announced acquisition

December 22nd, 2017 / Week 51 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com Highlight of the week was the announced acquisition

ORDERBOOK OBSERVER M A R C H

ORDERBOOK OBSERVER M A R C H 2 1 7 Tanker Orderbook by Builder Country Rank Country No. Mn Dwt Mn CGT Tanker Orders by Size Segment Share (%) of Total 1 South Korea 18 25.5 5. 38.8% 2 China 159 21.1 4.3

ORDERBOOK OBSERVER M A R C H 2 1 7 Tanker Orderbook by Builder Country Rank Country No. Mn Dwt Mn CGT Tanker Orders by Size Segment Share (%) of Total 1 South Korea 18 25.5 5. 38.8% 2 China 159 21.1 4.3

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) February 8th 2019 / Week 6

February 8th 2019 / Week 6") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 February 8th 2019 / Week 6 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 February 8th 2019 / Week 6 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Tanker Market Outlook

Tanker Market Outlook 4 th Maritime Indonesia Simon Chattrabhuti, Director, Head of Tanker Market Analysis Jakarta, 22 March 212 Disclaimer THIS PRESENTATION IS CONFIDENTIAL AND IS SOLELY FOR THE USE OF

Tanker Market Outlook 4 th Maritime Indonesia Simon Chattrabhuti, Director, Head of Tanker Market Analysis Jakarta, 22 March 212 Disclaimer THIS PRESENTATION IS CONFIDENTIAL AND IS SOLELY FOR THE USE OF

BUSINESS OVERVIEW FEBRUARY

BUSINESS OVERVIEW FEBRUARY 2018 Except for historical information, the statements made in this presentation constitute forward looking statements. These include statements regarding the intent, belief

BUSINESS OVERVIEW FEBRUARY 2018 Except for historical information, the statements made in this presentation constitute forward looking statements. These include statements regarding the intent, belief

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) September 7th 2018 / Week 36

September 7th 2018 / Week 36") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 September 7th 2018 / Week 36 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 September 7th 2018 / Week 36 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Future Trends in the Global Bunker Market

Future Trends in the Global Bunker Market Will Bathurst, Senior Analyst SSY Consultancy & Research Bunker Asia Forum Singapore, 7th Whilst care and attention has been taken to ensure that the information

Future Trends in the Global Bunker Market Will Bathurst, Senior Analyst SSY Consultancy & Research Bunker Asia Forum Singapore, 7th Whilst care and attention has been taken to ensure that the information

MALAYSIAN BULK CARRIERS BERHAD ( W)

") www.maybulk.com.my MALAYSIAN BULK CARRIERS BERHAD (175953-W) Contents t Commercial highlights Page 3 MBC Fleet composition 4 Shipping Revenue Composition and Operating Profit 5 MBC Fleet TCE rates 6 Fleet

www.maybulk.com.my MALAYSIAN BULK CARRIERS BERHAD (175953-W) Contents t Commercial highlights Page 3 MBC Fleet composition 4 Shipping Revenue Composition and Operating Profit 5 MBC Fleet TCE rates 6 Fleet

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) December 7th 2018 / Week 49

December 7th 2018 / Week 49") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 December 7th 2018 / Week 49 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 December 7th 2018 / Week 49 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

DRY BULK FREIGHT MARKET OUTLOOK MJUNCTION INDIAN STEEL MARKETS CONFERENCE

DRY BULK FREIGHT MARKET OUTLOOK MJUNCTION INDIAN STEEL MARKETS CONFERENCE JUNE 2018 PRESENTATION STRUCTURE where are we in the dry bulk freight market cycle? current freight rates in perspective fundamental

DRY BULK FREIGHT MARKET OUTLOOK MJUNCTION INDIAN STEEL MARKETS CONFERENCE JUNE 2018 PRESENTATION STRUCTURE where are we in the dry bulk freight market cycle? current freight rates in perspective fundamental

Global Oil&Gas Tanker Outlook

MARSEILLE MARITIME 28 Global Oil&Gas Tanker Outlook ( and just a few words on containerships) Ralph Leszczynski Marseille, 16 September 28 banchero costa research www.bancosta.it - research@bancosta.it

MARSEILLE MARITIME 28 Global Oil&Gas Tanker Outlook ( and just a few words on containerships) Ralph Leszczynski Marseille, 16 September 28 banchero costa research www.bancosta.it - research@bancosta.it

BUSINESS OVERVIEW 12 February 2019

BUSINESS OVERVIEW 12 February 2019 Except for historical information, the statements made in this presentation constitute forward looking statements. These include statements regarding the intent, belief

BUSINESS OVERVIEW 12 February 2019 Except for historical information, the statements made in this presentation constitute forward looking statements. These include statements regarding the intent, belief

Ahead in experience. Alfa Laval PureSOx references

Ahead in experience Alfa Laval PureSOx references Don t just comply be a step ahead You won t be alone in choosing a SOx scrubber. But you will be a step ahead, if you select the scrubber at the forefront:

Ahead in experience Alfa Laval PureSOx references Don t just comply be a step ahead You won t be alone in choosing a SOx scrubber. But you will be a step ahead, if you select the scrubber at the forefront:

December 15th, 2017 / Week 50 THE VIEW FROM THE BRIDGE. Full report can be viewed on the Market Reports tab at the following link:

December 15th, 2017 / Week 50 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com The BCI index moved slightly lower at the end of the

December 15th, 2017 / Week 50 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab at the following link: www.compassmar.com The BCI index moved slightly lower at the end of the

Future Marine Fuel Quality Changes: How might terminals prepare?

Future Marine Fuel Quality Changes: How might terminals prepare? Further reading from IHS: What Bunker Fuel for the High Seas? A global study on marine bunker fuel and how it can be supplied ABOUT IHS

Future Marine Fuel Quality Changes: How might terminals prepare? Further reading from IHS: What Bunker Fuel for the High Seas? A global study on marine bunker fuel and how it can be supplied ABOUT IHS

Product Tanker Market Outlook IMSF Geneva - May 2017

Product Tanker ket Outlook IMSF Geneva - 217 Global Presence 16 staff in strategic locations LONDON HOUSTON BEIJING SEOUL HONG KONG SINGAPORE Product Tanker ket Outlook 217 2 Where are we now? Product

Product Tanker ket Outlook IMSF Geneva - 217 Global Presence 16 staff in strategic locations LONDON HOUSTON BEIJING SEOUL HONG KONG SINGAPORE Product Tanker ket Outlook 217 2 Where are we now? Product

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) June 22nd, 2018 / Week 25 THE VIEW FROM THE BRIDGE

June 22nd, 2018 / Week 25 THE VIEW FROM THE BRIDGE") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 June 22nd, 2018 / Week 25 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 June 22nd, 2018 / Week 25 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Putting the Right Foot Forward: Strategies for Reducing Costs and Carbon Footprints

Putting the Right Foot Forward: Strategies for Reducing Costs and Carbon Footprints More than 140 years in business Business Segments: Maritime Classification, Maritime Solutions, Oil & Gas and Renewables

Putting the Right Foot Forward: Strategies for Reducing Costs and Carbon Footprints More than 140 years in business Business Segments: Maritime Classification, Maritime Solutions, Oil & Gas and Renewables

Commercial Highlights

1 3 Fleet Composition Tanker - as at 31 Dec Bulk Post-Panamax (5 vessels) 276,009 DWT Handysize (5 vessels) 435,260 DWT Supramax (5 Product Tanker (3 Carriers vessels) 156,302 DWT 142,129 DWT Grand-total

1 3 Fleet Composition Tanker - as at 31 Dec Bulk Post-Panamax (5 vessels) 276,009 DWT Handysize (5 vessels) 435,260 DWT Supramax (5 Product Tanker (3 Carriers vessels) 156,302 DWT 142,129 DWT Grand-total

EURONAV TALKS IMO 2020 FROM THE VIEW OF A SHIPOWNER JUNE

EURONAV TALKS IMO 2020 FROM THE VIEW OF A SHIPOWNER JUNE 2018 1 IMO 2020 2 % weight permitted WHAT IS IMO 2020 I HAVE SEEN ONE BEFORE.BUT NEVER THIS BIG Hill 4.5% Cliff 4.0% 3.5% 3.0% Open Seas 2.5% 2.0%

EURONAV TALKS IMO 2020 FROM THE VIEW OF A SHIPOWNER JUNE 2018 1 IMO 2020 2 % weight permitted WHAT IS IMO 2020 I HAVE SEEN ONE BEFORE.BUT NEVER THIS BIG Hill 4.5% Cliff 4.0% 3.5% 3.0% Open Seas 2.5% 2.0%

Implications Across the Supply Chain. Prepared for Sustainableshipping Conference San Francisco 30 September 2009

Implications Across the Supply Chain Prepared for Sustainableshipping Conference San Francisco 30 September 2009 Agenda Residual Markets & Quality Refinery Bunker Production Supply & Pricing 2 World marine

Implications Across the Supply Chain Prepared for Sustainableshipping Conference San Francisco 30 September 2009 Agenda Residual Markets & Quality Refinery Bunker Production Supply & Pricing 2 World marine

Marine Money - Odfjell SE. Leveraging an industrial platform to outperform the cycle

Marine Money - Odfjell SE Leveraging an industrial platform to outperform the cycle Odfjell SE - Key facts Established in 1914 Listed on Oslo Stock Exchange since 1986 One of the worlds largest operator

Marine Money - Odfjell SE Leveraging an industrial platform to outperform the cycle Odfjell SE - Key facts Established in 1914 Listed on Oslo Stock Exchange since 1986 One of the worlds largest operator

Outlook for Marine Bunkers and Fuel Oil to A key to understanding the future of marine bunkers and fuel oil markets

Outlook for Marine Bunkers and Fuel Oil to 2035 A key to understanding the future of marine bunkers and fuel oil markets 01 FGE & MECL 2014 Study completed by FGE and MECL FGE London FGE House 133 Aldersgate

Outlook for Marine Bunkers and Fuel Oil to 2035 A key to understanding the future of marine bunkers and fuel oil markets 01 FGE & MECL 2014 Study completed by FGE and MECL FGE London FGE House 133 Aldersgate

Trends for Refining Residual Fuel Oil. Prepared for Bunker Asia Forum 2011 Singapore 7 September 2011

Trends for Refining Residual Fuel Oil Prepared for Bunker Asia Forum 2011 Singapore 7 September 2011 Agenda Introduction Refiner View of Bunker Fuel Product Quality Crude Oil Influences Likely Refining

Trends for Refining Residual Fuel Oil Prepared for Bunker Asia Forum 2011 Singapore 7 September 2011 Agenda Introduction Refiner View of Bunker Fuel Product Quality Crude Oil Influences Likely Refining

Capital Link's 4th Annual Invest in International Shipping Forum. Dr Hermann J. Klein, Member of Executive Board of GL

Capital Link's 4th Annual Invest in International Shipping Forum The Added Value of Classification to Financial Institutions & Owners in Today's Capital Markets Dr Hermann J. Klein, Member of Executive

Capital Link's 4th Annual Invest in International Shipping Forum The Added Value of Classification to Financial Institutions & Owners in Today's Capital Markets Dr Hermann J. Klein, Member of Executive

Changes on the Horizon

2020 THE NEXT DAY A presentation by Captain Dimitrios MATTHEOU Managing Director of Arcadia Shipmanagement CO LTD & Aegean Bulk Chairman of GREEN AWARD Foundation 1 Changes on the Horizon Almost 100 years,

2020 THE NEXT DAY A presentation by Captain Dimitrios MATTHEOU Managing Director of Arcadia Shipmanagement CO LTD & Aegean Bulk Chairman of GREEN AWARD Foundation 1 Changes on the Horizon Almost 100 years,

A multi-fuel future: the impact of the IMO sulphur cap

6th Bunkernet Bunker Conference, 6 April 2017 A multi-fuel future: the impact of the IMO sulphur cap David Squirrell B.Eng, C.Eng, MIMechE, MBA Chief Engineer UK, Cyprus, and Middle East Please note that

6th Bunkernet Bunker Conference, 6 April 2017 A multi-fuel future: the impact of the IMO sulphur cap David Squirrell B.Eng, C.Eng, MIMechE, MBA Chief Engineer UK, Cyprus, and Middle East Please note that

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) October 26th 2018 / Week 43

October 26th 2018 / Week 43") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 October 26th 2018 / Week 43 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 October 26th 2018 / Week 43 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

Marine Insurance day 2018

Marine Insurance day 2018 Session, October 5, 2018 About McQuilling McQuilling Services is the marine transportation consulting and advisory group of McQuilling Partners, Inc. The primary focus of McQuilling

Marine Insurance day 2018 Session, October 5, 2018 About McQuilling McQuilling Services is the marine transportation consulting and advisory group of McQuilling Partners, Inc. The primary focus of McQuilling

Residual Fuel Market Issues

Residual Fuel Market Issues 26 February 2009 Kurt Barrow Crude Oil Quality Group Meeting Long Beach, CA Agenda Trends In Residue Demand IMO Bunker Regulations Implications for Shipping and Refining Industry

Residual Fuel Market Issues 26 February 2009 Kurt Barrow Crude Oil Quality Group Meeting Long Beach, CA Agenda Trends In Residue Demand IMO Bunker Regulations Implications for Shipping and Refining Industry

Q M c. McQuilling Services. Tanker Market Outlook Managing Performance in Extreme Markets. INTERTANKO Conference, Istanbul April 2008

Tanker Market Outlook Managing Performance in Extreme Markets INTERTANKO Conference, Istanbul April 2008 INTERTANKO, Istanbul, April 2008 Slide 1 2007: An Extreme Year Preface The Influence of Fundamentals

Tanker Market Outlook Managing Performance in Extreme Markets INTERTANKO Conference, Istanbul April 2008 INTERTANKO, Istanbul, April 2008 Slide 1 2007: An Extreme Year Preface The Influence of Fundamentals

The Great Eastern Shipping Co. Ltd. Business & Financial Review August 2011

The Great Eastern Shipping Co. Ltd. Business & Financial Review August 2011 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

The Great Eastern Shipping Co. Ltd. Business & Financial Review August 2011 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

Global LPG Shipping and Pricing Trending Topics. November

Global LPG Shipping and Pricing Trending Topics November 2017 1 Market snapshot Total LPG Production 305 million tons Highest ever level 5-year market growth 18% Twice as fast as crude oil growth Top Producer

Global LPG Shipping and Pricing Trending Topics November 2017 1 Market snapshot Total LPG Production 305 million tons Highest ever level 5-year market growth 18% Twice as fast as crude oil growth Top Producer

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ (201) January 11th 2019 / Week 2

January 11th 2019 / Week 2") GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 January 11th 2019 / Week 2 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

GLENPOINTE CENTRE WEST, FIRST FLOOR, 500 FRANK W. BURR BOULEVARD TEANECK, NJ 07666 (201) 907-0009 January 11th 2019 / Week 2 THE VIEW FROM THE BRIDGE Full report can be viewed on the Market Reports tab

All Aboard: The Dry Bulk Markets Changing Course. A Presentation to Global Grain Asia. by Janina Lam, Howe Robinson Shipbrokers

All Aboard: The Dry Bulk Markets Changing Course A Presentation to Global Grain Asia by Janina Lam, Howe Robinson Shipbrokers 12 th March 214 Index Value ( ) Baltic Dry Index 22 Today 12 BDI 9 BDI Annual

All Aboard: The Dry Bulk Markets Changing Course A Presentation to Global Grain Asia by Janina Lam, Howe Robinson Shipbrokers 12 th March 214 Index Value ( ) Baltic Dry Index 22 Today 12 BDI 9 BDI Annual

Marine Money Japan Ship Finance Forum

Marine Money Japan Ship Finance Forum Current Situation in Shipbuilding -World and Japan- Masashi Terakado The Shipbuilders Association of Japan May 12th, 2016 Contents 1. Current Situation and Projection

Marine Money Japan Ship Finance Forum Current Situation in Shipbuilding -World and Japan- Masashi Terakado The Shipbuilders Association of Japan May 12th, 2016 Contents 1. Current Situation and Projection

MDT TIER III options with low sulphur fuels

Greener Shipping Summit Athens, Greece, 10.11. 2015 MDT TIER III options with low sulphur fuels Michael Jeppesen Promotion Manager Sales & Customer Support Marine Low Speed < 1 > Agenda Greener Shipping

Greener Shipping Summit Athens, Greece, 10.11. 2015 MDT TIER III options with low sulphur fuels Michael Jeppesen Promotion Manager Sales & Customer Support Marine Low Speed < 1 > Agenda Greener Shipping

LNG fuel as an alternative to low-sulphur marine gas oil for complying with the new emission rules. September 29 th, 2017 Limassol

LNG fuel as an alternative to low-sulphur marine gas oil for complying with the new emission rules September 29 th, 2017 Limassol THE IMO S 2020 GLOBAL SULFUR CAP IMO sets 1 January 2020 for ships to comply

LNG fuel as an alternative to low-sulphur marine gas oil for complying with the new emission rules September 29 th, 2017 Limassol THE IMO S 2020 GLOBAL SULFUR CAP IMO sets 1 January 2020 for ships to comply

(with a review of fleets and trade) Ralph Leszczynski

Ralph Leszczynski") banchero costa Mareforum & Orecoal 4 th Iron Ore & Coal World Shipping Summit 2012 Dry Bulk Shipping Prospects (with a review of fleets and trade) Ralph Leszczynski 1 October 2012, Athens prepared by:

banchero costa Mareforum & Orecoal 4 th Iron Ore & Coal World Shipping Summit 2012 Dry Bulk Shipping Prospects (with a review of fleets and trade) Ralph Leszczynski 1 October 2012, Athens prepared by:

The Great Eastern Shipping Co. Ltd. Business & Financial Review June 2011

The Great Eastern Shipping Co. Ltd. Business & Financial Review June 2011 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

The Great Eastern Shipping Co. Ltd. Business & Financial Review June 2011 1 Forward Looking Statements Except for historical information, the statements made in this presentation constitute forward looking

Europe Far East Trade Product Changes from April March 29, 2018

Europe Far East Trade Product Changes from April 2018 March 29, 2018 Agenda 01 02 03 Trade Overview North Europe Far East Mediterranean Far East 01 North Trade Europe Overview North America Strengths of

Europe Far East Trade Product Changes from April 2018 March 29, 2018 Agenda 01 02 03 Trade Overview North Europe Far East Mediterranean Far East 01 North Trade Europe Overview North America Strengths of

Company Overview. Fleet Profile. Key Facts

STIFEL Conference Presentation February 12, 2019 Company Overview Scorpio Bulkers Inc. ( Scorpio or the Company ) owns or finance leases 56 mid-size dry bulk Eco vessels with an average age of 3.0 years

STIFEL Conference Presentation February 12, 2019 Company Overview Scorpio Bulkers Inc. ( Scorpio or the Company ) owns or finance leases 56 mid-size dry bulk Eco vessels with an average age of 3.0 years

AN ECONOMIC ASSESSMENT OF THE INTERNATIONAL MARITIME ORGANIZATION SULPHUR REGULATIONS

Study No. 175 CANADIAN ENERGY RESEARCH INSTITUTE AN ECONOMIC ASSESSMENT OF THE INTERNATIONAL MARITIME ORGANIZATION SULPHUR REGULATIONS ON MARKETS FOR CANADIAN CRUDE OIL Canadian Energy Research Institute

Study No. 175 CANADIAN ENERGY RESEARCH INSTITUTE AN ECONOMIC ASSESSMENT OF THE INTERNATIONAL MARITIME ORGANIZATION SULPHUR REGULATIONS ON MARKETS FOR CANADIAN CRUDE OIL Canadian Energy Research Institute

2020 Sulphur Cap. Challenges and Opportunities. Delivering Maritime Solutions.

2020 Sulphur Cap Challenges and Opportunities Delivering Maritime Solutions www.wallem.com About the Wallem Group Wallem Group is a maritime services company with headquarters in Hong Kong and an established

2020 Sulphur Cap Challenges and Opportunities Delivering Maritime Solutions www.wallem.com About the Wallem Group Wallem Group is a maritime services company with headquarters in Hong Kong and an established

The Tanker & Dry Cargo Outlook

Prof President, Clarkson Research The Tanker & Dry Cargo Outlook Mareforum, Rome Grand Hotel Parco dei Principi, Rome 8 th May 213 Quo Vadis? 1. Where are we now? 2. How do markets behave? 3. Where are

Prof President, Clarkson Research The Tanker & Dry Cargo Outlook Mareforum, Rome Grand Hotel Parco dei Principi, Rome 8 th May 213 Quo Vadis? 1. Where are we now? 2. How do markets behave? 3. Where are

The Impact of Shale Oil Production Growth in the US

The Impact of Shale Oil Production Growth in the US Presentation to IMSF, Copenhagen By Selena Yan, Senior Analyst www.clarksons.com Disclaimer The material and the information (including, without limitation,

The Impact of Shale Oil Production Growth in the US Presentation to IMSF, Copenhagen By Selena Yan, Senior Analyst www.clarksons.com Disclaimer The material and the information (including, without limitation,

BAZAN Group Oil Refineries Ltd. First Quarter 2014 Results. May 2014

BAZAN Group Oil Refineries Ltd. First Quarter 2014 Results May 2014 1 Disclaimer This presentation has been prepared by Oil Refineries Ltd. (the "Company") as a general presentation of the Company and

BAZAN Group Oil Refineries Ltd. First Quarter 2014 Results May 2014 1 Disclaimer This presentation has been prepared by Oil Refineries Ltd. (the "Company") as a general presentation of the Company and

2018 World Maritime Day Observance. November 14th, 2018 Cozumel, Quintana Roo, Mexico

2018 World Maritime Day Observance November 14th, 2018 Cozumel, Quintana Roo, Mexico Introduction Bulk Shipping de Mexico is an specialized company working as a consultant in Maritime Goods Carriage, established

2018 World Maritime Day Observance November 14th, 2018 Cozumel, Quintana Roo, Mexico Introduction Bulk Shipping de Mexico is an specialized company working as a consultant in Maritime Goods Carriage, established

Outlook for Marine Bunkers and Fuel Oil to 2025 Sourcing Lower Sulphur Products

Outlook for Marine Bunkers and Fuel Oil to 2025 Sourcing Lower Sulphur Products NOW AVAILABLE Increasing pressure from governments to address the issue of sulphur levels in ships bunkers has led IMO to

Outlook for Marine Bunkers and Fuel Oil to 2025 Sourcing Lower Sulphur Products NOW AVAILABLE Increasing pressure from governments to address the issue of sulphur levels in ships bunkers has led IMO to

European Power Workshop. David Goldsack Principal Coal Consultant, Global Energy Group

European Power Workshop David Goldsack Principal Coal Consultant, Global Energy Group Today s Presentation Upstream Coal Industry Transport Issues Contracting for Supplies Price Outlook Copyright 2007

European Power Workshop David Goldsack Principal Coal Consultant, Global Energy Group Today s Presentation Upstream Coal Industry Transport Issues Contracting for Supplies Price Outlook Copyright 2007

2020? Lars Robert Pedersen. Deputy Secretary General. EGCSA Conference London 22 May 2017

2020? Lars Robert Pedersen. Deputy Secretary General EGCSA Conference London 22 May 2017 Our vision To be the chosen partner trusted to provide leadership to the global shipping industry. Our mission To

2020? Lars Robert Pedersen. Deputy Secretary General EGCSA Conference London 22 May 2017 Our vision To be the chosen partner trusted to provide leadership to the global shipping industry. Our mission To

IMO 2020 & Marine Fuels An Oil Major s Viewpoint

Capital Link s 8 th Operational Excellence in Shipping Forum Oct 2018 IMO 2020 & Marine Fuels An Oil Major s Viewpoint Armelle Breneol ExxonMobil Marine Fuels Please note that the information in this document

Capital Link s 8 th Operational Excellence in Shipping Forum Oct 2018 IMO 2020 & Marine Fuels An Oil Major s Viewpoint Armelle Breneol ExxonMobil Marine Fuels Please note that the information in this document

Strategic Approach for Shipping Modernization In the Thailand

Strategic Approach for Shipping Modernization In the Thailand JETRO Singapore CAJS Japan Marine Science Inc. FEB. 2011 1 Ⅰ: Situation Summary Current Status and Issues Ⅱ: Key Elements for the development

Strategic Approach for Shipping Modernization In the Thailand JETRO Singapore CAJS Japan Marine Science Inc. FEB. 2011 1 Ⅰ: Situation Summary Current Status and Issues Ⅱ: Key Elements for the development

CMA Luncheon 23 February 2012

CMA Luncheon 23 February 2012 1 The Recycling Market Macro Matters Presented by: Bart Lawrence 2 SHIP RECYCLING - LOCATIONS Today s scrap markets (East to West) China, Bangladesh, India, Pakistan, Turkey

CMA Luncheon 23 February 2012 1 The Recycling Market Macro Matters Presented by: Bart Lawrence 2 SHIP RECYCLING - LOCATIONS Today s scrap markets (East to West) China, Bangladesh, India, Pakistan, Turkey

Workshop on GHG Emission On Ships Co-organised by CIL and MPA

Workshop on GHG Emission On Ships Co-organised by CIL and MPA By Simon Neo Regional Manager Asia International Bunker Industry Association 13 th -14 th Nov 2018 The Voice of the Global Bunker Industry

Workshop on GHG Emission On Ships Co-organised by CIL and MPA By Simon Neo Regional Manager Asia International Bunker Industry Association 13 th -14 th Nov 2018 The Voice of the Global Bunker Industry

1QFY2018 Financial Results. Quarter Ended 30 June 2017

1QFY2018 Financial Results Quarter Ended 30 June 2017 Disclaimer This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase, any

1QFY2018 Financial Results Quarter Ended 30 June 2017 Disclaimer This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase, any

The Tanker Sustainability Scenarios

Prof Martin Stopford President, Clarkson Research The Tanker Sustainability Scenarios Future view of tanker Industry Intertanko Sustainability Day Grand Hotel, Oslo, 30 th May 2013 1. A word about scenarios

Prof Martin Stopford President, Clarkson Research The Tanker Sustainability Scenarios Future view of tanker Industry Intertanko Sustainability Day Grand Hotel, Oslo, 30 th May 2013 1. A word about scenarios

Recent Developments in International Seaborne Trade and Maritime Transport

Recent Developments in International Seaborne Trade and Maritime Transport IFSPA, Hong Kong, 3-5 June 2013 Dr. Vincent F. Valentine Officer-in-Charge, Transport Section Division on Technology and Logistics

Recent Developments in International Seaborne Trade and Maritime Transport IFSPA, Hong Kong, 3-5 June 2013 Dr. Vincent F. Valentine Officer-in-Charge, Transport Section Division on Technology and Logistics

Shipping and Environmental Challenges MARINTEK 1

Shipping and Environmental Challenges 1 Development of World Energy Consumption 18000 16000 14000 12000 10000 8000 6000 4000 2000 0 World energy consumption 1975-2025 in MTOE 1970 1975 1980 1985 1990 1995

Shipping and Environmental Challenges 1 Development of World Energy Consumption 18000 16000 14000 12000 10000 8000 6000 4000 2000 0 World energy consumption 1975-2025 in MTOE 1970 1975 1980 1985 1990 1995

TANKER MARKET INSIGHT

TANKER MARKET INSIGHT June 18 Research Department, Strategic Development May-17 Jun-17 Jul-17 Sep-17 Oct-17 Dec-17 Jan-18 Mar-18 Apr-18 May-17 Jun-17 Jul-17 Sep-17 Oct-17 Dec-17 Jan-18 Mar-18 Apr-18 $

TANKER MARKET INSIGHT June 18 Research Department, Strategic Development May-17 Jun-17 Jul-17 Sep-17 Oct-17 Dec-17 Jan-18 Mar-18 Apr-18 May-17 Jun-17 Jul-17 Sep-17 Oct-17 Dec-17 Jan-18 Mar-18 Apr-18 $

The Study on Impacts of Market-based Measures for Greenhouse Gas Emission Reduction on Maritime Transport Costs

The Study on Impacts of Market-based Measures for Greenhouse Gas Emission Reduction on Maritime Transport Costs Weihong Gu 1*, Ruihua Xu 2 and Jie Zhao 3 1 College of Transportation Engineering, Tongji

The Study on Impacts of Market-based Measures for Greenhouse Gas Emission Reduction on Maritime Transport Costs Weihong Gu 1*, Ruihua Xu 2 and Jie Zhao 3 1 College of Transportation Engineering, Tongji

The environmental challenge ahead and The way forward. - Sulphur Cap 2020/ ECA zone - LNG as fuel

The environmental challenge ahead and The way forward - Sulphur Cap 2020/ ECA zone - LNG as fuel Yufeng Liu, Director Sales China Marine Money Shanghai, 10 th May 2017 Global sulphur Cap by 2020 A game

The environmental challenge ahead and The way forward - Sulphur Cap 2020/ ECA zone - LNG as fuel Yufeng Liu, Director Sales China Marine Money Shanghai, 10 th May 2017 Global sulphur Cap by 2020 A game

Tanker Market Outlook April 2018

Tanker ket Outlook il 218 Global Presence 16 staff in strategic locations LONDON HOUSTON BEIJING HONG KONG SINGAPORE Tanker ket Outlook il 218 2 218: Bottom of the crude tanker cycle? OPEC/non-OPEC production

Tanker ket Outlook il 218 Global Presence 16 staff in strategic locations LONDON HOUSTON BEIJING HONG KONG SINGAPORE Tanker ket Outlook il 218 2 218: Bottom of the crude tanker cycle? OPEC/non-OPEC production

How much oil are electric vehicles displacing?

How much oil are electric vehicles displacing? Aleksandra Rybczynska March 07, 2017 Executive summary EV s influence on global gasoline and diesel consumption is small but increasing quickly. This short

How much oil are electric vehicles displacing? Aleksandra Rybczynska March 07, 2017 Executive summary EV s influence on global gasoline and diesel consumption is small but increasing quickly. This short

Multipurpose & Heavy-Lift Fleet Update BreakBulk Europe 2016

Multipurpose & Heavy-Lift Fleet Update BreakBulk Europe 2016 26 th May 2016 Agenda: No let-up: MPV/HL Fleet still under siege Vessel Supply Multipurpose vessels and project carriers Cargo Demand Dry cargo

Multipurpose & Heavy-Lift Fleet Update BreakBulk Europe 2016 26 th May 2016 Agenda: No let-up: MPV/HL Fleet still under siege Vessel Supply Multipurpose vessels and project carriers Cargo Demand Dry cargo

3QFY2018 Financial Results. Quarter Ended 31 December 2017

3QFY2018 Financial Results Quarter Ended 31 December 2017 Disclaimer This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase,

3QFY2018 Financial Results Quarter Ended 31 December 2017 Disclaimer This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase,

Handelsbanken s. 5 th Transport Seminar. Billede. Michael Tønnes Jørgensen Executive Vice President & CFO. (Solnedgang?)

") Handelsbanken s Billede 5 th Transport Seminar (Solnedgang?) 2010 Michael Tønnes Jørgensen Executive Vice President & CFO October 2010 THE PREFERRED PARTNER IN GLOBAL TRAMP SHIPPING. UNIQUE PEOPLE. OPEN

Handelsbanken s Billede 5 th Transport Seminar (Solnedgang?) 2010 Michael Tønnes Jørgensen Executive Vice President & CFO October 2010 THE PREFERRED PARTNER IN GLOBAL TRAMP SHIPPING. UNIQUE PEOPLE. OPEN

The Changing composition of bunker fuels: Implications for refiners, traders, and shipping

Platts 4 th European Refining Markets Conference The Changing composition of bunker fuels: Implications for refiners, traders, and shipping Wade DeClaris, EVP Marine World Fuel Services Corp. Agenda: Role

Platts 4 th European Refining Markets Conference The Changing composition of bunker fuels: Implications for refiners, traders, and shipping Wade DeClaris, EVP Marine World Fuel Services Corp. Agenda: Role

EXPANSION OF THE PANAMA CANAL AND ITS IMPACT ON TANKERS. José Ramón Arango S. Liquid Bulk Segment October 4th 2017

EXPANSION OF THE PANAMA CANAL AND ITS IMPACT ON TANKERS José Ramón Arango S. Liquid Bulk Segment October 4th 2017 Agenda Panama Canal Expansion Panama Canal Expansion Performance Impact of the Expansion

EXPANSION OF THE PANAMA CANAL AND ITS IMPACT ON TANKERS José Ramón Arango S. Liquid Bulk Segment October 4th 2017 Agenda Panama Canal Expansion Panama Canal Expansion Performance Impact of the Expansion

Market outlook for the Breakbulk & Heavy-Lift sector BreakBulk Americas 2016

Market outlook for the Breakbulk & Heavy-Lift sector BreakBulk Americas 2016 29th September 2016 Agenda: Blue Water Blues: Fleet Outlook Vessel Supply Multipurpose vessels and project carriers Cargo Demand

Market outlook for the Breakbulk & Heavy-Lift sector BreakBulk Americas 2016 29th September 2016 Agenda: Blue Water Blues: Fleet Outlook Vessel Supply Multipurpose vessels and project carriers Cargo Demand

Market Briefing: Mergers & Acquisitions World, Region, & Country

Market Briefing: Mergers & Acquisitions World, Region, & Country January 2, 217 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Please visit our sites at www. blog. thinking outside

Market Briefing: Mergers & Acquisitions World, Region, & Country January 2, 217 Dr. Edward Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-36 jabbott@ Please visit our sites at www. blog. thinking outside

Fuel Oil Sulfur Spreads Set to Widen Through 2020 Regulations upend bunker fuel market.

? Fuel Oil Sulfur Spreads Set to Widen Through 2020 Regulations upend bunker fuel market. Morningstar Commodities Research June 11, 2018 Sandy Fielden Director, Oil and Products Research +1 512 431-8044

? Fuel Oil Sulfur Spreads Set to Widen Through 2020 Regulations upend bunker fuel market. Morningstar Commodities Research June 11, 2018 Sandy Fielden Director, Oil and Products Research +1 512 431-8044

AN INTEGRATED GROUP. A single point of contact for a full spectrum of solutions

AN INTEGRATED GROUP Exploration & Production Refining & Chemicals Marketing & Services Gas Renewable & Power Trading & Shipping Total Marine Fuels Global Solutions is a dedicated M&S business unit: with

AN INTEGRATED GROUP Exploration & Production Refining & Chemicals Marketing & Services Gas Renewable & Power Trading & Shipping Total Marine Fuels Global Solutions is a dedicated M&S business unit: with

Competitive Edge through Environmental Performance

Competitive Edge through Environmental Performance Bo Cerup-Simonsen, Vice President Ph.D. Naval Architect, MBA Shipping & Logistics Blue Event no. 23 - Copenhagen, 3rd February 2011 (MMT) is a highly

Competitive Edge through Environmental Performance Bo Cerup-Simonsen, Vice President Ph.D. Naval Architect, MBA Shipping & Logistics Blue Event no. 23 - Copenhagen, 3rd February 2011 (MMT) is a highly

Changes in Bunker Fuel Quality Impact on European and Russian Refiners

Changes in Bunker Fuel Quality Impact on European and Russian Refiners Russia & CIS Bottom of the Barrel Technology Conference 23 &24 April 2015, Moscow Euro Petroleum Consultants TABLE OF CONTENT Requirements

Changes in Bunker Fuel Quality Impact on European and Russian Refiners Russia & CIS Bottom of the Barrel Technology Conference 23 &24 April 2015, Moscow Euro Petroleum Consultants TABLE OF CONTENT Requirements

Shipbuilding Statistics APRIL, 2017

Shipbuilding Statistics APRIL, 2017 Contents: Shipbuilding Statistics (APRIL, 2017) 1. World New Orders... 1 2. World Completions... 2 3. World Orderbook at Year-End... 3 4. World Merchant Fleets by Ship

Shipbuilding Statistics APRIL, 2017 Contents: Shipbuilding Statistics (APRIL, 2017) 1. World New Orders... 1 2. World Completions... 2 3. World Orderbook at Year-End... 3 4. World Merchant Fleets by Ship

Aegean Marine Petroleum Network Inc.

Aegean Marine Petroleum Network Inc. First Quarter 2007 Conference Call May 24, 2007 Disclosure Today s s presentation and discussion will contain forward-looking statements within the meaning of the Private

Aegean Marine Petroleum Network Inc. First Quarter 2007 Conference Call May 24, 2007 Disclosure Today s s presentation and discussion will contain forward-looking statements within the meaning of the Private

Residual Fuel Market Outlook

Residual Fuel Market Outlook Colin Birch Prepared for EGCSA workshop Hamburg 8/9 September 2010 Vice President Purvin & Gertz study is based on a scenario analysis to understand impact on refining industry

Residual Fuel Market Outlook Colin Birch Prepared for EGCSA workshop Hamburg 8/9 September 2010 Vice President Purvin & Gertz study is based on a scenario analysis to understand impact on refining industry

9M 2003 Financial Results (US GAAP)

") 9M Financial Results (US GAAP) January 2004 LUKOIL Group Crude Oil Production* mln tonnes 82 80 78 76 74 72 70 68 66 64 Crude oil production 3.2 5.5 3.9 76.8 70.3 71.3 2001 Production by subsidiaries Share

9M Financial Results (US GAAP) January 2004 LUKOIL Group Crude Oil Production* mln tonnes 82 80 78 76 74 72 70 68 66 64 Crude oil production 3.2 5.5 3.9 76.8 70.3 71.3 2001 Production by subsidiaries Share

Q Analyst Teleconference. 9 August 2018

9 August 218 Disclaimer This presentation contains forward-looking statements that reflect the Company management s current views with respect to certain future events. Although it is believed that the

9 August 218 Disclaimer This presentation contains forward-looking statements that reflect the Company management s current views with respect to certain future events. Although it is believed that the

Shipbuilding Statistics SEPTEMBER, 2018

Shipbuilding Statistics SEPTEMBER, 2018 Contents: Shipbuilding Statistics (SEPTEMBER, 2018) 1. World New Orders... 1 2. World Completions... 2 3. World Orderbook at Year-End... 3 4. World Merchant Fleets

Shipbuilding Statistics SEPTEMBER, 2018 Contents: Shipbuilding Statistics (SEPTEMBER, 2018) 1. World New Orders... 1 2. World Completions... 2 3. World Orderbook at Year-End... 3 4. World Merchant Fleets

Energy Briefing: World Crude Oil Outlays & Revenues

Energy Briefing: World Crude Oil Outlays & Revenues y 31, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites

Energy Briefing: World Crude Oil Outlays & Revenues y 31, 217 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites

Perception is everything make sure that you can discover the illusion

Perception is everything make sure that you can discover the illusion Fuel savings Compared to what & how to measure? Almost all suppliers to the marine industry offers fuel / emission savings but can

Perception is everything make sure that you can discover the illusion Fuel savings Compared to what & how to measure? Almost all suppliers to the marine industry offers fuel / emission savings but can

US Economic Indicators: Merchandise Trade

US Economic Indicators: Merchandise Trade July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

US Economic Indicators: Merchandise Trade July 6, 218 Dr. Edward Yardeni 516-972-7683 eyardeni@ Debbie Johnson 48-664-1333 djohnson@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www.

Developments in China s methanol market and implications for global supply Seoul

Developments in China s methanol market and implications for global supply Seoul Anu Agarwal 8 May 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing

Developments in China s methanol market and implications for global supply Seoul Anu Agarwal 8 May 2015 London Houston Washington New York Portland Calgary Santiago Bogota Rio de Janeiro Singapore Beijing

Marine Division. Peter Leifland Alfa Laval Group

Marine Division Peter Leifland Alfa Laval Group Alfa Slide Laval 2 Marine Division by numbers - Order intake (OI) based on LTM September 30, 2018, Order intake: SEK Bn 16.5 (+39%*) Split by type of orders

Marine Division Peter Leifland Alfa Laval Group Alfa Slide Laval 2 Marine Division by numbers - Order intake (OI) based on LTM September 30, 2018, Order intake: SEK Bn 16.5 (+39%*) Split by type of orders

Opening keynote: Setting the scene the shipowners and shipmanagers point of view

IBIA Annual Convention Hamburg 2014 04 November 2014, Hamburg Dr Hermann J. Klein, CEO E.R. Schiffahrt Opening keynote: Setting the scene the shipowners and shipmanagers point of view Change of shipping

IBIA Annual Convention Hamburg 2014 04 November 2014, Hamburg Dr Hermann J. Klein, CEO E.R. Schiffahrt Opening keynote: Setting the scene the shipowners and shipmanagers point of view Change of shipping

Global Index Briefing: MSCI Sectors Forward P/Es Selected Countries & Regions

Global Index Briefing: Selected Countries & Regions July 18, 18 Dr. Ed Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-6 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog.

Global Index Briefing: Selected Countries & Regions July 18, 18 Dr. Ed Yardeni 16-972-7683 eyardeni@ Joe Abbott 732-497-6 jabbott@ Mali Quintana 48-664-1333 aquintana@ Please visit our sites at www. blog.

Laivanrakennuksen kilpailutekijät tulevaisuudessa- vanha toimiala, uudet kujeet Jari Anttila, STX Finland

Laivanrakennuksen kilpailutekijät tulevaisuudessa- vanha toimiala, uudet kujeet 15-16.1.2013 Jari Anttila, STX Finland Index New vessels in the horizon How to reduce emissions with design LNG as a fuel

Laivanrakennuksen kilpailutekijät tulevaisuudessa- vanha toimiala, uudet kujeet 15-16.1.2013 Jari Anttila, STX Finland Index New vessels in the horizon How to reduce emissions with design LNG as a fuel

METHANOL SHIPPING: SAILING TOWARDS NEW HORIZONS 19 TH IMPCA ASIAN METHANOL CONFERENCE QUINCANNON ASIA PTE LTD KARAN GROVER

METHANOL SHIPPING: 19 TH IMPCA ASIAN METHANOL CONFERENCE SAILING TOWARDS NEW HORIZONS 2 3 NOVEMBER, 2016 SINGAPORE QUINCANNON ASIA PTE LTD KARAN GROVER 2 AGENDA METHANOL TRADE DYNAMICS IN BRIEF METHANOL

METHANOL SHIPPING: 19 TH IMPCA ASIAN METHANOL CONFERENCE SAILING TOWARDS NEW HORIZONS 2 3 NOVEMBER, 2016 SINGAPORE QUINCANNON ASIA PTE LTD KARAN GROVER 2 AGENDA METHANOL TRADE DYNAMICS IN BRIEF METHANOL

Inland Truck Shortage in North America. February 2018

Inland Truck Shortage in North America February 2018 1 Inland Truck Shortage in North America Continues Industry is experiencing severe truck shortages in certain locations in North America Challenges

Inland Truck Shortage in North America February 2018 1 Inland Truck Shortage in North America Continues Industry is experiencing severe truck shortages in certain locations in North America Challenges

Challenges for sustainable freight transport Maritime transport. Elena Seco Gª Valdecasas Director Spanish Shipowners Association - ANAVE

Challenges for sustainable freight transport Maritime transport Elena Seco Gª Valdecasas Director Spanish Shipowners Association - ANAVE Index 1. Shipping air emissions vs other transport modes. 2. How

Challenges for sustainable freight transport Maritime transport Elena Seco Gª Valdecasas Director Spanish Shipowners Association - ANAVE Index 1. Shipping air emissions vs other transport modes. 2. How

YULON MOTOR CO., LTD. Investor Conference

TW:2201 YULON MOTOR CO., LTD. Investor Conference 2017/11/23 人 車 生活 Disclaimer Statement 1. This document is provided by Yulon Motor Co., Ltd. (the Company"). Except for the numbers and information included

TW:2201 YULON MOTOR CO., LTD. Investor Conference 2017/11/23 人 車 生活 Disclaimer Statement 1. This document is provided by Yulon Motor Co., Ltd. (the Company"). Except for the numbers and information included

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 22nd August, 11 Volume 371 Week 34 Sale & Purchase Activity Week 34 SECOND HAND SALES DRY TONNAGE

OPTIMA SHIPBROKERS LTD Sales & Purchase / Dry Cargo Chartering Tanker Chartering / Newbuildings Monday 22nd August, 11 Volume 371 Week 34 Sale & Purchase Activity Week 34 SECOND HAND SALES DRY TONNAGE

Q3 Interim Report 2016

Q3 Interim Report 216 Lennart Evrell President & CEO Håkan Gabrielsson CFO Strong earnings and high mine production Revenues 9,733 (9,764) MSEK EBIT ex PIR* 1,318 (1,55) MSEK EBIT 1,529 (88) MSEK Free

Q3 Interim Report 216 Lennart Evrell President & CEO Håkan Gabrielsson CFO Strong earnings and high mine production Revenues 9,733 (9,764) MSEK EBIT ex PIR* 1,318 (1,55) MSEK EBIT 1,529 (88) MSEK Free