Refining An Overview

|

|

|

- Dennis Gallagher

- 5 years ago

- Views:

Transcription

1 An Overview October 2014

2 Industry Upstream - It involves the exploration for and extraction of petroleum crude oil and natural gas. The upstream oil sector is also known as the exploration and production (E&P) sector. Midstream - The midstream involves storing, marketing and transporting petroleum crude oil,natural gas. Midstream operations aresometimes included in the downstream category. Downstream - The downstream sector includes petroleum refineries, petroleum product distribution, retail outlets and natural gas distribution companies.

3 mln tonnes World Oil Reserves 145, , , ,204 World Consumption (annual) 3,162 3,584 4,040 4,185 World Production (annual) 3,175 3,620 3,979 4,133 Largest Consumer USA mln tonnes China mln tonnes Largest Producer Saudi Arabia mln tonnes Russia mln tonnes Largest Reserves Venezuela - 46,576 mln tonnes Saudi Arabia - 36,518 mln tonnes

4 Jargon Over 195 different types of s API Gravity: American Institute Gravity, which is a measure that compares how light or heavy a crude oil is in relation to water. If an oils API Gravity is greater than 10 then it is lighter than water and will float on it. If an oils API Gravity is less than 10, it is heavier than water and will sinks. West Texas Intermediate: also known as Texas Light Sweet is a light crude oil. API Gravity of 39.6 degrees, 0.24% sulfur content Brent Blend: a combination of different oils from 15 fields throughout the Scottish Brent and Ninian systems located in the North Sea. API Gravity is 38.3 degrees, 0.37 percent sulfur content OPEC Basket: The acronym OPEC stands for Organization of -Exporting Countries which is an organization that was formed in 1960 in order to create some common policy for the production and sale of oil within its jurisdiction. Comprises 11 member countries crude stream. API Gravity is 32.7 degrees, 1.77 percent sulfur content

5 000' mln tonnes World Reserves North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific Total

6 mln tonnes mln tones World Production 1,600 4,800 1,400 4,200 1,200 3,600 1,000 3, , , , North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific World Production

7 mln tonnes mln tones World Consumption 1,600 4,800 1,400 4,200 1,200 3,600 1,000 3, , , , North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific World Consumption -

8 USD / bbl 160 Price Comparison WTI and Brent Brent Crude WTI

9 Global Trade In mln tons

10

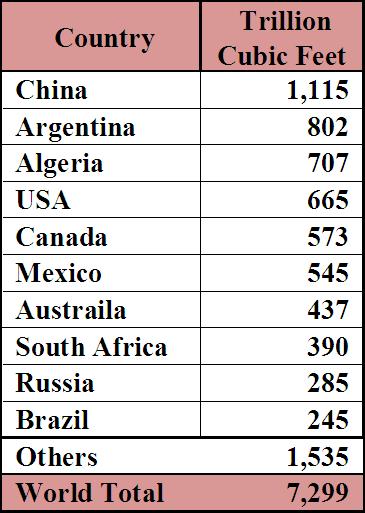

11 & Shale Gas ly Recoverable Reserves Shale Gas

3,706")

12 Global Capacities (mln tonnes) 3,706 4,094 4,572 4,727 YoY 10.5% 11.7% 3.4%

13 Process } Light Distillates } Medium Distillates } Heavy Distillates

14 Types of Topping - The topping refinery just separates the crude into its constituent petroleum products by distillation, known as Atmospheric Distillation. Topping Refinery produces naphtha but no gasoline. Hydroskimming - The hydroskimming refinery is equipped with Atmospheric Distillation, naphtha reforming and necessary treating processes. Hydroskimming refinery is more complex than a topping refinery and it produces gasoline. Cracking - The cracking refinery, in addition to the above, is equipped with vacuum distillation and catalytic cracking. The cracking refinery reduces fuel oil by conversion to light distillates and middle distillates. Coking - The coking refinery is equipped to process the vacuum residue into high value products using the Delayed Coking Process. The coking refinery adds further complexity to the cracking refinery by high conversion offuel oil into distillates and petroleum coke. Nelson Complexity Index - The Nelson Complexity Index typically varies from about 2 for Hydroskimming refineries, to about 5 for the Cracking refineries and over 9 for the Coking refineries., with high Nelson Complexity Index have the necessary flexibility in processing a wide variety of crudes and are capable of achieving higher value addition.

15 mln tonnes mln tones Global Capacities 1,600 4,800 1,400 4,200 1,200 3,600 1,000 3, , , , North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific Global Capacities Global Capacities (mln tonnes) 4,572 4,591 4,658 4,727 YoY 1.1% 0.4% 1.5% 1.5%

16 %age %age Regional Capacity Utilization 90% 90% 80% 80% 70% 70% 60% 60% 50% North America South & Central America Europe & Eurasia Middle East Africa Asia Pacific Global Capacity Utilization 50%

17 Global Refined Products Trade In mln tons

18 s

19 Lube Oil Jargon Viscosity Index? Used to measure the thickness of liquid. High for thin liquids and low for thick, which means, The higher the VI, the less an oil will thicken as it gets cold and the less it will thin out at higher temperatures providing better lubricant performance at both temperature extremes. 11% 9% 30% 50% Group I Group II Group III Group IV & V

20 Global Demand ~38.6mln tonnes Europe: Oversupplied market Low prices. pressure on margins Weak demand Capacity expansion Threat from the US supply North America: Demand Driver: USA Shift towards Group II World s largest refinery coming online may create a supply glut Net exporter Middle East: Demand Driver: Industrialization and vehicle growth ~15% expected growth in lube demand Rising capacities 17% 8% 7% 25% 43% Asia North America Europe Middle East Others Asia: Majorly driven by developing economies like China & India Stable supply since no planned maintenance Expected urbanization in China expected to support the lube market Govt. restriction on vehicle purchase may hinder the demand

21 Margins Margins still under pressure post Baltic Sea glut problems. Going forward, the margins are expected to remain under pressure owing to the extensive capacity expansion, which is expected to rise by ~3.5mln tonnes per annum by 2014.

22 Capacity Expansion

23

24 % age mln barrels Recoverable Reserves 100% 9% 2% 1% 7% 9% % 9% 8% 8% 11% 8% 10% % 20% 15% 14% % % 51% 60% 58% 80 0% OGDCL MOL PPL POL UEPL Others Total -

25 % age mln barrels Crude Production 100% 80% 5% 6% 5% 13% 10% 15% 5% 4% 3% 10% 10% 9% % 11% 12% 14% 18 40% 12 56% 57% 54% 20% 6 0% OGDCL MOL PPL POL UEPL Others Total -

26

27 Capacity & Utilization Refinery Capactity Utilization Capactity Utilization Capactity Utilization Expansion Byco % % % - Pak Arab Refinery % % % - National Refinery % % % - Pakistan Refinery % % % - Attock Refinery % % % 0.5 ENAR Petrotech % % % - Dhodak Refinery % Total % % % 0.5 Without Byco %

28 mln tonnes Processed POL Imports Imported Crude Local Crude

29 Percentage Product Mix 100% 80% 4% 4% 4% 5% 5% 4% 9% 8% 7% 9% 8% 7% 13% 14% 14% 60% 26% 25% 26% 40% 20% 34% 36% 37% 0% HSD FO Motor Spirit Aviation Fuel Naphta Non Energy Products Other Energy Products

30 % age mln tonnes Supply Demand Mix Fuels 100% 10 80% 44% 52% 57% 50% 44% 46% 25% 23% 33% 8 60% 6 40% 20% 56% 48% 43% 50% 56% 54% 75% 77% 67% 4 2 0% HSD Motor Spirit Furnace Oil Imports Local Consumption

31

32 Exchange Rate Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Exchange Gain Rate / Loss 1, QFY14 2QFY14 3QFY14 4QFY14 (500) (1,000) (1,500) PARCO NRL ARL PRL

33 Impact of Regulatory Duty Government of Attock National Pak Pakistan Byco Country's FY13 Pakistan Refinery Refinery Arab Refinery Collection Sector (Imports) (ARL) (NRL) Refinery (PRL) Pakistan Sale of HSD (Thousand Tonnes) 6,820 2,954 3, (PARCO 1, (Byco) 290 Conversion to Liters (Mln Liters) 8,149 3,530 4, , Average Ex-Refinery Price (PKR/Liter) Total Revenue (PKR Mln) 507, , ,592 41,177 53, ,128 45,159 21,538 Deemed Duty on HSD - 7.5% (PKR Mln) 38,049 16,479 21,569 3,088 4,044 9,235 3,387 1,615 Profitability (PKR Mln) 27,580 2,627 3,520 19,950 1,482 Profitability excluding deemed duty (PKR Mln) 6,010 (461) (524) 10,716 (1,905) Deemed Duty increase from FY16-9% (PKR Mln) 7,610 3,296 4, ,

34 Price Disclosure Particulars (Rs/ Litre) HSD (Diesel) PMG (Petrol) Retail Direct Retail Direct LDO Ex Refinery Price Levy Inland Freight Equalization Margin Dealer Commission Distribution Margin Ex Depot Price Sales Tax Maximum Ex Depot Price

35 Key Risks Volatility in margins an outcome of fluctuating crude oil prices and simpler technology Unfavorable changes in pricing regime removal of deemed duty Prevailing Inter-Corporate Debt impacting throughput levels Exchange rate depreciation What s the outlook Stable

36 Bibliography 1. Pakistan Energy Year Book : Attock Limited: Product Prices 3. Attock Refinery Limited Annual & Quarterly Financial Statements Sep13, Dec13, Mar14, Jun14 4. BP Statistical Review of World Energy 2013: bp.com 5. US Energy Information Administration 6. Bain & Company: Global 7. zedatawatch: A Brief History of Oil Prices and Middle East Tensions: Fear of a Black Gold Shortage 8. Oil Price History and Analysis: 9. The Economist: ICIS Base Oil Review Argus Base Oil Report Kline & Company 13. Fuels & Lube : Lube Report: Ernst & Young - The international dynamics of shale 16. Ernst & Young -Shale gas in Europe: Revolution or evolution? 17. KPMG -Shale Development: Global Update 18. PricewaterhouseCoopers, the next energy resolution 19. Deloitte University Press- US shale: A game of choices 20. Oxford Business Group 21.

37 Analysts Rai Umar Zafar Manager Ratings Muhammad Siddiq Senior Financial Analyst Suffiyan Saleem Financial Analyst DISCLAIMER PACRA has used due care in preparation of this document. Our information has been obtained from sources we consider to be reliable but its accuracy or completeness is not guaranteed. The information in this document may be copied or otherwise reproduced, in whole or in part, provided the source is duly acknowledged. The presentation should not be relied upon as professional advice.

Pakistan Refining Industry An Overview

Pakistan Refining Industry An Overview October 2016 Oil World Crude Oil Reserves Largely sustained level of reserves Largest Region Contributes 47% (2014: 47.2%) Global proven oil reserves in 2015 fell

Pakistan Refining Industry An Overview October 2016 Oil World Crude Oil Reserves Largely sustained level of reserves Largest Region Contributes 47% (2014: 47.2%) Global proven oil reserves in 2015 fell

An Overview on Pakistan Refining Industry

An Overview on Pakistan Refining Industry May 2018 Oil 000' mln tonnes World Crude Oil Reserves 120,000 240,000 Largely sustained level of reserves 90,000 225,000 Middle east Contributes ~48% 60,000 210,000

An Overview on Pakistan Refining Industry May 2018 Oil 000' mln tonnes World Crude Oil Reserves 120,000 240,000 Largely sustained level of reserves 90,000 225,000 Middle east Contributes ~48% 60,000 210,000

Refineries Table of Contents

Refineries Dec 18 Refineries Table of Contents Refineries Table of Contents Contents: Page # National Fuel Consumption Product Wise 3 Demand and Supply POL Products 4 Local Refineries POL Volume Sales

Refineries Dec 18 Refineries Table of Contents Refineries Table of Contents Contents: Page # National Fuel Consumption Product Wise 3 Demand and Supply POL Products 4 Local Refineries POL Volume Sales

Oil Marketing Companies

Oil Marketing Companies May 2016 National Fuel Product Wise The country s petroleum products consumption have shown a rising trend over the past few years. Declining furnace oil consumption led to a fall

Oil Marketing Companies May 2016 National Fuel Product Wise The country s petroleum products consumption have shown a rising trend over the past few years. Declining furnace oil consumption led to a fall

Oil Marketing Companies

Oil Marketing Companies December 2017 % age '000 tonnes National Fuel Product Wise 10 8 6 4% 4% 5% 4% 45% 41% 38% 37% 35,000 28,000 21,000 The country s petroleum products consumption have shown a rising

Oil Marketing Companies December 2017 % age '000 tonnes National Fuel Product Wise 10 8 6 4% 4% 5% 4% 45% 41% 38% 37% 35,000 28,000 21,000 The country s petroleum products consumption have shown a rising

Abstract Process Economics Program Report 222 PETROLEUM INDUSTRY OUTLOOK (July 1999)

") Abstract Process Economics Program Report 222 PETROLEUM INDUSTRY OUTLOOK (July 1999) Global energy demand is rising, with fossil fuels oil, natural gas, and coal continuing to provide more than 90% of

Abstract Process Economics Program Report 222 PETROLEUM INDUSTRY OUTLOOK (July 1999) Global energy demand is rising, with fossil fuels oil, natural gas, and coal continuing to provide more than 90% of

Methodology. Supply. Demand

Methodology Supply Demand Tipping the Scale 1 Overview Latin America and the Caribbean, a major petroleum product importing region, provides an important counterbalance to surpluses in refined product

Methodology Supply Demand Tipping the Scale 1 Overview Latin America and the Caribbean, a major petroleum product importing region, provides an important counterbalance to surpluses in refined product

Thursday, March 6, 2014 Houston, TX. 8:30 9:40 a.m. AN ECONOMIST S-EYE VIEW OF THE ENERGY INDUSTRY: HYDROCARBON HAT TRICK

Thursday, March 6, 214 Houston, TX 8:3 9:4 a.m. AN ECONOMIST S-EYE VIEW OF THE ENERGY INDUSTRY: HYDROCARBON HAT TRICK Presented by Jesse Thompson Business Economist Federal Reserve Bank of Dallas, Houston

Thursday, March 6, 214 Houston, TX 8:3 9:4 a.m. AN ECONOMIST S-EYE VIEW OF THE ENERGY INDUSTRY: HYDROCARBON HAT TRICK Presented by Jesse Thompson Business Economist Federal Reserve Bank of Dallas, Houston

PAKISTAN ENERGY CONFERENCE 2016

PAKISTAN ENERGY CONFERENCE 2016 PAKISTAN ENERGY MIX Pakistan s Annual GDP growth 4.2% in 2014-15 Pakistan s Energy Mix During FY14-15 Hydro, Nuclear & Others, 13.40% Coal, 5.40% LPG, 0.50% Gas, 46.30%

PAKISTAN ENERGY CONFERENCE 2016 PAKISTAN ENERGY MIX Pakistan s Annual GDP growth 4.2% in 2014-15 Pakistan s Energy Mix During FY14-15 Hydro, Nuclear & Others, 13.40% Coal, 5.40% LPG, 0.50% Gas, 46.30%

A summary of national and global energy indicators. FEDERAL RESERVE BANK of KANSAS CITY

THE U.S. Energy DATABOOK A summary of national and global energy indicators JULY 1, 17 FEDERAL RESERVE BANK of KANSAS CITY SUMMARY OF CURRENT ENERGY CONDITIONS The number of total active drilling rigs

THE U.S. Energy DATABOOK A summary of national and global energy indicators JULY 1, 17 FEDERAL RESERVE BANK of KANSAS CITY SUMMARY OF CURRENT ENERGY CONDITIONS The number of total active drilling rigs

Regional Refining Outlook

Regional Refining Outlook Implications for Crude Demand Platts Crude Summit 15 May 213 David Wech JBC Energy GmbH 13 th May 213 Research - Energy Studies - Consulting - Training Disclaimer All statements

Regional Refining Outlook Implications for Crude Demand Platts Crude Summit 15 May 213 David Wech JBC Energy GmbH 13 th May 213 Research - Energy Studies - Consulting - Training Disclaimer All statements

CHEMSYSTEMS. Report Abstract. Petrochemical Market Dynamics Feedstocks

CHEMSYSTEMS PPE PROGRAM Report Abstract Petrochemical Market Dynamics Feedstocks Petrochemical feedstocks industry overview, crude oil, natural gas, coal, biological hydrocarbons, olefins, aromatics, methane

CHEMSYSTEMS PPE PROGRAM Report Abstract Petrochemical Market Dynamics Feedstocks Petrochemical feedstocks industry overview, crude oil, natural gas, coal, biological hydrocarbons, olefins, aromatics, methane

Petroleum Planning & Analysis Cell

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS September 2018 Petroleum Planning & Analysis Cell (Ministry of Petroleum &

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS September 2018 Petroleum Planning & Analysis Cell (Ministry of Petroleum &

1H 2003 Financial Results (US GAAP)

") 1H 2003 Financial Results (US GAAP) October 2003 Crude Oil Production Growth bpd 1.52 1.50 1.48 1.46 1.44 1.42 1.40 Jan- 03 Daily crude production Feb- 03 Mar- 03 Apr- 03 May- 03 Jun- 03 Crude oil production*

1H 2003 Financial Results (US GAAP) October 2003 Crude Oil Production Growth bpd 1.52 1.50 1.48 1.46 1.44 1.42 1.40 Jan- 03 Daily crude production Feb- 03 Mar- 03 Apr- 03 May- 03 Jun- 03 Crude oil production*

Where Are Oil Prices Headed? Graham Loveland Senior Consultant, Oil

Resource Scramble or Market Rebalance: Where Are Oil Prices Headed? Graham Loveland Senior Consultant, Oil Presentation Outline & Approach Outline Key messages Demand Supply Costs & Prices Refining & Products

Resource Scramble or Market Rebalance: Where Are Oil Prices Headed? Graham Loveland Senior Consultant, Oil Presentation Outline & Approach Outline Key messages Demand Supply Costs & Prices Refining & Products

Q Analyst Teleconference. 9 August 2018

9 August 218 Disclaimer This presentation contains forward-looking statements that reflect the Company management s current views with respect to certain future events. Although it is believed that the

9 August 218 Disclaimer This presentation contains forward-looking statements that reflect the Company management s current views with respect to certain future events. Although it is believed that the

RESULTS FOR Q ANALYST TELECONFERENCE

RESULTS FOR Q4 216 ANALYST TELECONFERENCE Market 1 2 Operation Financials 3 Market 1 216 Fourth Quarter Market Conditions Product Market Crude Oil Postponed Maintenances Started to take place High Agricultural

RESULTS FOR Q4 216 ANALYST TELECONFERENCE Market 1 2 Operation Financials 3 Market 1 216 Fourth Quarter Market Conditions Product Market Crude Oil Postponed Maintenances Started to take place High Agricultural

Petroleum Planning & Analysis Cell

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS November 2017 Petroleum Planning & Analysis Cell (Ministry of Petroleum &

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS November 2017 Petroleum Planning & Analysis Cell (Ministry of Petroleum &

2015 Interim Results Announcement

China Petroleum & Chemical Corporation 2015 Interim Results Announcement August 27, 2015 Hong Kong Cautionary Statement This presentation and the presentation materials distributed herein include forward-looking

China Petroleum & Chemical Corporation 2015 Interim Results Announcement August 27, 2015 Hong Kong Cautionary Statement This presentation and the presentation materials distributed herein include forward-looking

Global Downstream Petroleum Outlook

Global Downstream Petroleum Outlook Claude Mandil Executive Director International Energy Agency 3 rd OPEC International Seminar Vienna, 12 September 26 Spare Refinery Capacity Has Tightened 9 1% 85 95%

Global Downstream Petroleum Outlook Claude Mandil Executive Director International Energy Agency 3 rd OPEC International Seminar Vienna, 12 September 26 Spare Refinery Capacity Has Tightened 9 1% 85 95%

Fuel Focus. Understanding Gasoline Markets in Canada and Economic Drivers Influencing Prices. Issue 20, Volume 8

Fuel Focus Understanding Gasoline Markets in Canada and Economic Drivers Influencing Prices Issue 20, Volume 8 October 18, 2013 Copies of this publication may be obtained free of charge from: Natural Resources

Fuel Focus Understanding Gasoline Markets in Canada and Economic Drivers Influencing Prices Issue 20, Volume 8 October 18, 2013 Copies of this publication may be obtained free of charge from: Natural Resources

OPEC PRIMARY ENERGY CONSUMPTION IN 2005 (1)

") CHAPTER 4 I n 1384, political tensions in the Middle East and some oil-producing countries, sabotage in Iraq s oil industry and speculation in the market raised oil prices incrementally. As of the beginning

CHAPTER 4 I n 1384, political tensions in the Middle East and some oil-producing countries, sabotage in Iraq s oil industry and speculation in the market raised oil prices incrementally. As of the beginning

Emerging Trends in Petroleum Markets

Emerging Trends in Petroleum Markets For Defense Logistics Agency, Worldwide Energy Conference Washington, D.C. By T. Mason Hamilton, Petroleum Markets Analyst U.S. Energy Information Administration Independent

Emerging Trends in Petroleum Markets For Defense Logistics Agency, Worldwide Energy Conference Washington, D.C. By T. Mason Hamilton, Petroleum Markets Analyst U.S. Energy Information Administration Independent

Oil Refining in a CO 2 Constrained World Implications for Gasoline & Diesel Fuels

Oil Refining in a CO 2 Constrained World Implications for Gasoline & Diesel Fuels Amir F.N. Abdul-Manan & Hassan Babiker Strategic Transport Analysis Team (STAT), Saudi Aramco Agenda 1. Global Mobility

Oil Refining in a CO 2 Constrained World Implications for Gasoline & Diesel Fuels Amir F.N. Abdul-Manan & Hassan Babiker Strategic Transport Analysis Team (STAT), Saudi Aramco Agenda 1. Global Mobility

2010 Interim Results Presentation. August 23, 2010 Hong Kong

Sinopec Corp. 21 Interim Results Presentation August 23, 21 Hong Kong Disclaimer i This presentation and the presentation materials distributed herein include forwardlooking statements. All statements,

Sinopec Corp. 21 Interim Results Presentation August 23, 21 Hong Kong Disclaimer i This presentation and the presentation materials distributed herein include forwardlooking statements. All statements,

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products Second Meeting of the EU Refining Forum Brussels, 27 November 2013 Toril Bosoni, International Energy Agency OECD/IEA

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products Second Meeting of the EU Refining Forum Brussels, 27 November 2013 Toril Bosoni, International Energy Agency OECD/IEA

Petroleum Planning & Analysis Cell

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS May 2018 Petroleum Planning & Analysis Cell (Ministry of Petroleum & Natural

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS May 2018 Petroleum Planning & Analysis Cell (Ministry of Petroleum & Natural

Fuel Focus. Understanding Gasoline Markets in Canada and Economic Drivers Influencing Prices. Issue 24, Volume 8

Fuel Focus Understanding Gasoline Markets in Canada and Economic Drivers Influencing Prices Issue 24, Volume 8 December, Copies of this publication may be obtained free of charge from: Natural Resources

Fuel Focus Understanding Gasoline Markets in Canada and Economic Drivers Influencing Prices Issue 24, Volume 8 December, Copies of this publication may be obtained free of charge from: Natural Resources

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: January 16, 2019 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 120 100 Brent (Jan 11 = $58.64) WTI (Jan 11 = $50.78)

ENERGY SLIDESHOW Updated: January 16, 2019 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 120 100 Brent (Jan 11 = $58.64) WTI (Jan 11 = $50.78)

9M 2003 Financial Results (US GAAP)

") 9M Financial Results (US GAAP) January 2004 LUKOIL Group Crude Oil Production* mln tonnes 82 80 78 76 74 72 70 68 66 64 Crude oil production 3.2 5.5 3.9 76.8 70.3 71.3 2001 Production by subsidiaries Share

9M Financial Results (US GAAP) January 2004 LUKOIL Group Crude Oil Production* mln tonnes 82 80 78 76 74 72 70 68 66 64 Crude oil production 3.2 5.5 3.9 76.8 70.3 71.3 2001 Production by subsidiaries Share

OCTANE THE NEW ECONOMICS OF. What Drives the Cost of Octane and Why Octane Costs Have Risen Since 2012 T. J. HIGGINS. A Report By:

THE NEW ECONOMICS OF OCTANE What Drives the Cost of Octane and Why Octane Costs Have Risen Since 2012 A Report By: T. J. HIGGINS Contents Foreword... 1 1. Executive Summary... 2 2. Tracking the Changing

THE NEW ECONOMICS OF OCTANE What Drives the Cost of Octane and Why Octane Costs Have Risen Since 2012 A Report By: T. J. HIGGINS Contents Foreword... 1 1. Executive Summary... 2 2. Tracking the Changing

Global Refining: Fueling Profitability in the Turbulent Times Ahead. Sponsored by:

Global Refining: Fueling Profitability in the Turbulent Times Ahead Sponsored by: The Outlook for Energy: A View to 24 Roland L. Moreau ExxonMobil Upstream Research Company Hart Energy Breakfast Club February

Global Refining: Fueling Profitability in the Turbulent Times Ahead Sponsored by: The Outlook for Energy: A View to 24 Roland L. Moreau ExxonMobil Upstream Research Company Hart Energy Breakfast Club February

Petroleum Planning & Analysis Cell

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS February 2018 Petroleum Planning & Analysis Cell (Ministry of Petroleum &

MONTHLY REPORT ON INDIGENOUS CRUDE OIL PRODUCTION, IMPORT AND PROCESSING & PRODUCTION, IMPORT AND EXPORT OF PETROLEUM PRODUCTS February 2018 Petroleum Planning & Analysis Cell (Ministry of Petroleum &

Gas & electricity - at a glance

$/barrel /tco 2 e p/therm /MWh Gas & electricity - at a glance Week-on-Week Annual Gas Price Changes Short-term gas contracts jump Cold snap forecast for the first half of February, lifting demand Longer-dated

$/barrel /tco 2 e p/therm /MWh Gas & electricity - at a glance Week-on-Week Annual Gas Price Changes Short-term gas contracts jump Cold snap forecast for the first half of February, lifting demand Longer-dated

Market Report Series: Oil 2018 Analysis & Forecasts to Energy Community 10 th Oil Forum, Belgrade, 25 September 2018

Market Report Series: Oil 218 Analysis & Forecasts to 223 Energy Community 1 th Oil Forum, Belgrade, 25 September 218 Short term update: crude prices (excl. WTI) up strongly Aug/Sep $/bbl 8 Benchmark Crude

Market Report Series: Oil 218 Analysis & Forecasts to 223 Energy Community 1 th Oil Forum, Belgrade, 25 September 218 Short term update: crude prices (excl. WTI) up strongly Aug/Sep $/bbl 8 Benchmark Crude

New York Energy Forum

Presentation at the New York Energy Forum 30 June 2014 Antoine Halff The oil market at a junction Balances loosen up on paper but must be seen in perspective The unconventional supply revolution enters

Presentation at the New York Energy Forum 30 June 2014 Antoine Halff The oil market at a junction Balances loosen up on paper but must be seen in perspective The unconventional supply revolution enters

POINTS TO COVER UNCONVENTIONAL OIL AND GAS AND THE SHALE REVOLUTION: GAME CHANGER 4/16/2014. If we don t screw it up! Context Implications Risks

UNCONVENTIONAL OIL AND GAS AND THE SHALE REVOLUTION: GAME CHANGER If we don t screw it up! POINTS TO COVER Context Implications Risks April 11 1 You can always count on Americans to do the right thing

UNCONVENTIONAL OIL AND GAS AND THE SHALE REVOLUTION: GAME CHANGER If we don t screw it up! POINTS TO COVER Context Implications Risks April 11 1 You can always count on Americans to do the right thing

ANNUAL STATISTICAL SUPPLEMENT

ANNUAL STATISTICAL SUPPLEMENT with 2016 data 2017 Edition This Statistical Supplement has been prepared to provide a longer historical perspective for the oil demand, supply, trade, stocks, prices and

ANNUAL STATISTICAL SUPPLEMENT with 2016 data 2017 Edition This Statistical Supplement has been prepared to provide a longer historical perspective for the oil demand, supply, trade, stocks, prices and

Growing Latin America: Feedstocks and Competitiveness

MIDSTREAM DOWNSTREAM CHEMICAL Presentation Growing Latin America: Feedstocks and Competitiveness November 216 ihsmarkit.com Dr. Nick Rados, Global Business Director, Feedstocks +1 832 619 8593, nick.rados@ihsmarkit.com

MIDSTREAM DOWNSTREAM CHEMICAL Presentation Growing Latin America: Feedstocks and Competitiveness November 216 ihsmarkit.com Dr. Nick Rados, Global Business Director, Feedstocks +1 832 619 8593, nick.rados@ihsmarkit.com

Welcome Welcome... 1

Welcome Welcome... 1 Presentation Structure Our presentation is split into three sections going through the market, operations and financials 2 3 As it has been indicated previously, it is now much clear

Welcome Welcome... 1 Presentation Structure Our presentation is split into three sections going through the market, operations and financials 2 3 As it has been indicated previously, it is now much clear

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: March 13, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Mar 9 = $65.12) WTI (Mar 9 = $61.65) 120 100

ENERGY SLIDESHOW Updated: March 13, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Mar 9 = $65.12) WTI (Mar 9 = $61.65) 120 100

The road leading to the 0.50% sulphur limit and IMO s role moving forward

The road leading to the 0.50% sulphur limit and IMO s role moving forward 2020 global sulphur challenge Copenhagen, 21 March 2017 Dr Edmund Hughes Marine Environment Division International Maritime Organization

The road leading to the 0.50% sulphur limit and IMO s role moving forward 2020 global sulphur challenge Copenhagen, 21 March 2017 Dr Edmund Hughes Marine Environment Division International Maritime Organization

- Supercritical Water Cracking Technology -

JOGMEC Techno Forum 2014, November 26 th -27 th 2014 Upgrading of Heavy Crude Oil - Technology - Hisato Aoyama Manager, Technology Development Center JGC CORPORATION Organization--Background The Super

JOGMEC Techno Forum 2014, November 26 th -27 th 2014 Upgrading of Heavy Crude Oil - Technology - Hisato Aoyama Manager, Technology Development Center JGC CORPORATION Organization--Background The Super

Downstream Petroleum Sector The Growing Prominence of Asian Refining

Downstream Petroleum Sector The Growing Prominence of Asian Refining Mr. Fahad Al-Dihani Deputy CEO,MAA Refinery, Kuwait National Petroleum Company-Kuwait Outline.. Global refining trends Kuwait s Position

Downstream Petroleum Sector The Growing Prominence of Asian Refining Mr. Fahad Al-Dihani Deputy CEO,MAA Refinery, Kuwait National Petroleum Company-Kuwait Outline.. Global refining trends Kuwait s Position

ASPHALT SUPPLY IN A VOLATILE OIL WORLD. Bill Haverland ConocoPhillips Company

ASPHALT SUPPLY IN A VOLATILE OIL WORLD Bill Haverland ConocoPhillips Company Issues to be Discussed Crude Oil Supply Crude Oil Pricing Refining Capacity Products Supply Products Pricing Future of the Industry

ASPHALT SUPPLY IN A VOLATILE OIL WORLD Bill Haverland ConocoPhillips Company Issues to be Discussed Crude Oil Supply Crude Oil Pricing Refining Capacity Products Supply Products Pricing Future of the Industry

Mr. Steve Jenkins Head Global PX and Derivatives PCI X&P Malaysia

Mr. Steve Jenkins Head Global PX and Derivatives PCI X&P Malaysia Recognized as a leading global authority in the commercial analysis of the paraxylene and derivatives industry sector, Mr. Steve Jenkins,

Mr. Steve Jenkins Head Global PX and Derivatives PCI X&P Malaysia Recognized as a leading global authority in the commercial analysis of the paraxylene and derivatives industry sector, Mr. Steve Jenkins,

B A K E R & O B R I E N

B A K E R & O B R I E N I N C O R P O R A T E D Q3 : U. S. Refining Margins Remain Robust Special Topic: Domestic Light Oil Processing in the U.S. Gulf Coast Have We Hit the Limit? Houston, October 30,

B A K E R & O B R I E N I N C O R P O R A T E D Q3 : U. S. Refining Margins Remain Robust Special Topic: Domestic Light Oil Processing in the U.S. Gulf Coast Have We Hit the Limit? Houston, October 30,

ANNUAL STATISTICAL SUPPLEMENT

ANNUAL STATISTICAL SUPPLEMENT with 2008 data 2009 Edition This Statistical Supplement has been prepared to provide a longer historical perspective for the oil demand, supply, trade, stocks, prices and

ANNUAL STATISTICAL SUPPLEMENT with 2008 data 2009 Edition This Statistical Supplement has been prepared to provide a longer historical perspective for the oil demand, supply, trade, stocks, prices and

Methodology and specifications guide China Oil Analytics

Methodology and specifications guide China Oil Analytics Latest update: March 2018 Scope of service 2 Contact us 2 Frequency of publication 2 Frequency of data updates 2 Data and analysis sources 2 Forecasting

Methodology and specifications guide China Oil Analytics Latest update: March 2018 Scope of service 2 Contact us 2 Frequency of publication 2 Frequency of data updates 2 Data and analysis sources 2 Forecasting

Focus on Refinery Product Flows

December 14, 2016 Focus on Refinery Product Flows Stratas Advisors Gasoline Imports in 2014 CIS and the Middle East are the largest gasoline exporters to Asia. While China and India do not import gasoline

December 14, 2016 Focus on Refinery Product Flows Stratas Advisors Gasoline Imports in 2014 CIS and the Middle East are the largest gasoline exporters to Asia. While China and India do not import gasoline

DOWNSTREAM PETROLEUM 2017 DOWNSTREAM PETROLEUM

DOWNSTREAM PETROLEUM International and Asian Refining The global refining industry is fundamentally changing as emerging and maturing trends re-shape the global supply and demand patterns for crude oil

DOWNSTREAM PETROLEUM International and Asian Refining The global refining industry is fundamentally changing as emerging and maturing trends re-shape the global supply and demand patterns for crude oil

Nove b m er 21, Yun K Kan g Jessie i Y Yoh

Energy for tomorrow November 21, 2008 Yun Kang Jessie Yoh Industry Overview Company Overview Thesis Analysis Risks Q & A AGENDA WHY CONOCO? Leader in refining process provides natural hedge against falling

Energy for tomorrow November 21, 2008 Yun Kang Jessie Yoh Industry Overview Company Overview Thesis Analysis Risks Q & A AGENDA WHY CONOCO? Leader in refining process provides natural hedge against falling

ASPHALT SUPPLY IN A VOLATILE OIL WORLD. Bill Haverland ConocoPhillips Company

ASPHALT SUPPLY IN A VOLATILE OIL WORLD Bill Haverland ConocoPhillips Company Issues to be Discussed Crude Oil Supply Crude Oil Pricing Refining Capacity Products Supply Products Pricing Future of the Industry

ASPHALT SUPPLY IN A VOLATILE OIL WORLD Bill Haverland ConocoPhillips Company Issues to be Discussed Crude Oil Supply Crude Oil Pricing Refining Capacity Products Supply Products Pricing Future of the Industry

Petroleum and Natural Gas Situation

Petroleum and Natural Gas Situation John C. Felmy Chief Economist and Director Statistics Department American Petroleum Institute Felmyj@api.org www.api.org www.gasolineandyou.org www.naturalgasfacts.org

Petroleum and Natural Gas Situation John C. Felmy Chief Economist and Director Statistics Department American Petroleum Institute Felmyj@api.org www.api.org www.gasolineandyou.org www.naturalgasfacts.org

Downstream & Chemicals

Downstream & Chemicals Pierre Breber Executive Vice President 017 Chevron Corporation Downstream portfolio Fuels refining & marketing Integrated value chains Lubricants & additives Globally positioned

Downstream & Chemicals Pierre Breber Executive Vice President 017 Chevron Corporation Downstream portfolio Fuels refining & marketing Integrated value chains Lubricants & additives Globally positioned

Implications Across the Supply Chain. Prepared for Sustainableshipping Conference San Francisco 30 September 2009

Implications Across the Supply Chain Prepared for Sustainableshipping Conference San Francisco 30 September 2009 Agenda Residual Markets & Quality Refinery Bunker Production Supply & Pricing 2 World marine

Implications Across the Supply Chain Prepared for Sustainableshipping Conference San Francisco 30 September 2009 Agenda Residual Markets & Quality Refinery Bunker Production Supply & Pricing 2 World marine

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products Third Meeting of the EU Refining Forum Brussels, 22 May 2014 Toril Bosoni, International Energy Agency OECD/IEA 2014

Recent Developments in EU Refining and in the Supply and Trade of Petroleum Products Third Meeting of the EU Refining Forum Brussels, 22 May 2014 Toril Bosoni, International Energy Agency OECD/IEA 2014

AN ECONOMIC ASSESSMENT OF THE INTERNATIONAL MARITIME ORGANIZATION SULPHUR REGULATIONS

Study No. 175 CANADIAN ENERGY RESEARCH INSTITUTE AN ECONOMIC ASSESSMENT OF THE INTERNATIONAL MARITIME ORGANIZATION SULPHUR REGULATIONS ON MARKETS FOR CANADIAN CRUDE OIL Canadian Energy Research Institute

Study No. 175 CANADIAN ENERGY RESEARCH INSTITUTE AN ECONOMIC ASSESSMENT OF THE INTERNATIONAL MARITIME ORGANIZATION SULPHUR REGULATIONS ON MARKETS FOR CANADIAN CRUDE OIL Canadian Energy Research Institute

The Changing Face of Global Refining

The Changing Face of Global Refining OPIS National Supply Summit Las Vegas, Nevada October 24-26, 2010 John B. O Brien, Executive Chairman Baker & O Brien, Inc. All rights reserved. The Changing Face of

The Changing Face of Global Refining OPIS National Supply Summit Las Vegas, Nevada October 24-26, 2010 John B. O Brien, Executive Chairman Baker & O Brien, Inc. All rights reserved. The Changing Face of

U.S. Crude Exports and Impact on Trade

U.S. Crude Exports and Impact on Trade 32 nd Annual Asia Pacific Petroleum Conference Dr. Helen Currie Senior Economist September 7, 2016 Cautionary Statement The following presentation includes forward-looking

U.S. Crude Exports and Impact on Trade 32 nd Annual Asia Pacific Petroleum Conference Dr. Helen Currie Senior Economist September 7, 2016 Cautionary Statement The following presentation includes forward-looking

Sulphur Market Outlook

Sulphur Market Outlook The Outlook for the future Supply and Balance of the Global Sulphur Market Joanne Peacock, CRU International/BSC Creon Moscow December 2009 LONDON RALEIGH WASHINGTON MINNEAPOLIS

Sulphur Market Outlook The Outlook for the future Supply and Balance of the Global Sulphur Market Joanne Peacock, CRU International/BSC Creon Moscow December 2009 LONDON RALEIGH WASHINGTON MINNEAPOLIS

Medium-term Coal Market Report 2011 Carlos Fernández Alvarez. Senior Coal Analyst. Gas, Coal and Power Markets Division

Medium-term Coal Market Report 211 Carlos Fernández Alvarez. Senior Coal Analyst. Gas, Coal and Power Markets Division Madrid, 31 January 212 The context Uncertainties will fundamentally shape the medium-term

Medium-term Coal Market Report 211 Carlos Fernández Alvarez. Senior Coal Analyst. Gas, Coal and Power Markets Division Madrid, 31 January 212 The context Uncertainties will fundamentally shape the medium-term

A perspective on the refining industry. Platts European Refining Summit Brussels, 29 September2016 Kristine Petrosyan, International Energy Agency

A perspective on the refining industry Platts European Refining Summit Brussels, 29 September2016 Kristine Petrosyan, International Energy Agency OECD/IEA 2016 mb/d European refiners: busy 2015 OECD Europe

A perspective on the refining industry Platts European Refining Summit Brussels, 29 September2016 Kristine Petrosyan, International Energy Agency OECD/IEA 2016 mb/d European refiners: busy 2015 OECD Europe

PERSPECTIVES FOR THE BRAZILIAN REFINING INDUSTRY

PERSPECTIVES FOR THE BRAZILIAN REFINING INDUSTRY Jorge Celestino Refining & Natural Gas Executive Director 24.10.2016 Transformations facing the oil industry Changes in the competitive scenario: shale

PERSPECTIVES FOR THE BRAZILIAN REFINING INDUSTRY Jorge Celestino Refining & Natural Gas Executive Director 24.10.2016 Transformations facing the oil industry Changes in the competitive scenario: shale

Energy Security of APEC Economies in a Changing Downstream Oil Environment

IEEJ Feb. 2018 4th APEC OGSN Forum on 7 March 2018 Session2-2 Energy Security of APEC Economies in a Changing Downstream Oil Environment Takashi MATSUMOTO and Ichiro KUTANI Manager, Global Energy Group

IEEJ Feb. 2018 4th APEC OGSN Forum on 7 March 2018 Session2-2 Energy Security of APEC Economies in a Changing Downstream Oil Environment Takashi MATSUMOTO and Ichiro KUTANI Manager, Global Energy Group

Sinopec Corp. Q Results Announcement. 29 October 2010

Sinopec Corp. Q3 2010 Results Announcement 29 October 2010 Disclaimer i As required by the CSRC, financial statements of the third quarter of Sinopec Corp. (the Company ) were prepared under PRC Accounting

Sinopec Corp. Q3 2010 Results Announcement 29 October 2010 Disclaimer i As required by the CSRC, financial statements of the third quarter of Sinopec Corp. (the Company ) were prepared under PRC Accounting

April Título da apresentação DD.MM.AAAA

Aquisition of Shell Argentina downstream assets April 2018 Título da apresentação DD.MM.AAAA DISCLAIMER This presentation contains estimates and forward-looking statements regarding our strategy and opportunities

Aquisition of Shell Argentina downstream assets April 2018 Título da apresentação DD.MM.AAAA DISCLAIMER This presentation contains estimates and forward-looking statements regarding our strategy and opportunities

Tanker Market Outlook

Tanker Market Outlook 4 th Maritime Indonesia Simon Chattrabhuti, Director, Head of Tanker Market Analysis Jakarta, 22 March 212 Disclaimer THIS PRESENTATION IS CONFIDENTIAL AND IS SOLELY FOR THE USE OF

Tanker Market Outlook 4 th Maritime Indonesia Simon Chattrabhuti, Director, Head of Tanker Market Analysis Jakarta, 22 March 212 Disclaimer THIS PRESENTATION IS CONFIDENTIAL AND IS SOLELY FOR THE USE OF

Consulting and Training Services Available to the Petroleum Industry

Consulting and Training Services Available to the Petroleum Industry Iraj Isaac Rahmim, PhD, Inc. Houston, Texas, USA Crude Oil Quality Group Chateau Sonesta Hotel New Orleans January 2005 Products and

Consulting and Training Services Available to the Petroleum Industry Iraj Isaac Rahmim, PhD, Inc. Houston, Texas, USA Crude Oil Quality Group Chateau Sonesta Hotel New Orleans January 2005 Products and

Issues to be Discussed ASPHALT SUPPLY IN A VOLATILE OIL WORLD. Crude Oil Supply (2006) CRUDE OIL SUPPLY. Crude Oil Demand CRUDE OIL PRICING

CRUDE OIL SUPPLY. Crude Oil Demand CRUDE OIL PRICING") 6 SEAUPG CONFERENCE - WILMINGN, NORTH CAROLINA Issues to be Discussed ASPHALT SUPPLY IN A VOLATILE OIL WORLD Bill Haverland ConocoPhillips Company Crude Oil Supply Crude Oil Pricing Refining Capacity Products

6 SEAUPG CONFERENCE - WILMINGN, NORTH CAROLINA Issues to be Discussed ASPHALT SUPPLY IN A VOLATILE OIL WORLD Bill Haverland ConocoPhillips Company Crude Oil Supply Crude Oil Pricing Refining Capacity Products

Trinidad and Tobago Energy

Trinidad and Tobago Energy Conference 2017 Advantages of Vertical Integration in a Low Oil Price Environment Astor Harris Vice President Refining and Marketing 2017 January 24 Market Fundamentals 1Q13

Trinidad and Tobago Energy Conference 2017 Advantages of Vertical Integration in a Low Oil Price Environment Astor Harris Vice President Refining and Marketing 2017 January 24 Market Fundamentals 1Q13

How the U.S. transformed its crude oil import streams

How the U.S. transformed its crude oil import streams or How I learnt to stop worrying about increasing U.S. domestic crude production and embrace increased tonne miles, new export markets for traditional

How the U.S. transformed its crude oil import streams or How I learnt to stop worrying about increasing U.S. domestic crude production and embrace increased tonne miles, new export markets for traditional

Operating Expenses and Margin Analysis of the European Union (EU) Refineries vs Regional Peers

Refineries vs Regional Peers") Operating Expenses and Margin Analysis of the European Union (EU) Refineries vs Regional Peers Tracy Ellerington Third Meeting of the EU Refining Forum 22 May 214 Solomon Benchmarking Global Standard We

Operating Expenses and Margin Analysis of the European Union (EU) Refineries vs Regional Peers Tracy Ellerington Third Meeting of the EU Refining Forum 22 May 214 Solomon Benchmarking Global Standard We

Global Refining : Delivering Long-Term Value

Taking on the world s toughest energy challenges. Global Refining : Delivering Long-Term Value J. Steve Simon Sr. Vice President, Exxon Mobil Corporation Goldman Sachs Global Energy Conference January

Taking on the world s toughest energy challenges. Global Refining : Delivering Long-Term Value J. Steve Simon Sr. Vice President, Exxon Mobil Corporation Goldman Sachs Global Energy Conference January

INTERTANKO Istanbul Tanker Event. Demand Developments. David Martin Oil Industry & Markets Division OECD/IEA

INTERTANKO Istanbul Tanker Event Demand Developments David Martin Industry & s Division david.martin@iea.org - Istanbul, April 20-23, 2008 Medium-Term Outlook What is driving oil prices? Fundamentals or

INTERTANKO Istanbul Tanker Event Demand Developments David Martin Industry & s Division david.martin@iea.org - Istanbul, April 20-23, 2008 Medium-Term Outlook What is driving oil prices? Fundamentals or

Downstream & Chemicals

Downstream & Chemicals Pierre Breber Executive Vice President Profitable downstream & chemicals portfolio Fuels refining & marketing Focused, regional optimization Petrochemicals Advantaged feed, scale

Downstream & Chemicals Pierre Breber Executive Vice President Profitable downstream & chemicals portfolio Fuels refining & marketing Focused, regional optimization Petrochemicals Advantaged feed, scale

European Energy Union Impact on the Refining & Petrochemical Business. John Cooper, Director General Budapest, 13th October 2015

European Energy Union Impact on the Refining & Petrochemical Business John Cooper, Director General Budapest, 13th October 2015 FuelsEurope represents 42 Member Companies 100% of EU Refining Page 2 AGENDA

European Energy Union Impact on the Refining & Petrochemical Business John Cooper, Director General Budapest, 13th October 2015 FuelsEurope represents 42 Member Companies 100% of EU Refining Page 2 AGENDA

Petroplus. Overview & Outlook: Independent Refining February 17, 2009

Petroplus Overview & Outlook: Independent Refining February 17, 29 Disclaimer While all reasonable care has been taken to ensure that the facts stated herein are accurate and that the opinions contained

Petroplus Overview & Outlook: Independent Refining February 17, 29 Disclaimer While all reasonable care has been taken to ensure that the facts stated herein are accurate and that the opinions contained

The Impact of Shale Oil Production Growth in the US

The Impact of Shale Oil Production Growth in the US Presentation to IMSF, Copenhagen By Selena Yan, Senior Analyst www.clarksons.com Disclaimer The material and the information (including, without limitation,

The Impact of Shale Oil Production Growth in the US Presentation to IMSF, Copenhagen By Selena Yan, Senior Analyst www.clarksons.com Disclaimer The material and the information (including, without limitation,

4 th April, 2018 I Industry Research

April'17 May'17 June'17 July'17 August'17 September'17 October'17 November'17 December'17 January'18 February'18 March'18 A case for including Petrol and Diesel under GST? Contact: Madan Sabnavis Chief

April'17 May'17 June'17 July'17 August'17 September'17 October'17 November'17 December'17 January'18 February'18 March'18 A case for including Petrol and Diesel under GST? Contact: Madan Sabnavis Chief

Downstream & Chemicals

Downstream & Chemicals Mark Nelson Executive Vice President Downstream & chemicals portfolio Fuels refining & marketing Focused, regional optimization Petrochemicals Advantaged feed, scale and technology

Downstream & Chemicals Mark Nelson Executive Vice President Downstream & chemicals portfolio Fuels refining & marketing Focused, regional optimization Petrochemicals Advantaged feed, scale and technology

Energy Outlook. U.S. Energy Information Administration. For EnerCom Dallas February 22, 2018 Dallas, TX

Energy Outlook For EnerCom Dallas Dallas, TX Jeff Barron Industry Economist, U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

Energy Outlook For EnerCom Dallas Dallas, TX Jeff Barron Industry Economist, U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

The Oil and Gas Sector

Yuriy Bobylev The Oil and Gas Sector The world market in was characterized by the persistence of high global oil and natural gas prices. The average price of Russian Urals crude oil on the European market,

Yuriy Bobylev The Oil and Gas Sector The world market in was characterized by the persistence of high global oil and natural gas prices. The average price of Russian Urals crude oil on the European market,

Refineries, Product Market and Capacity Expansion Opportunities and Outlook in India- 2018

Refineries, Product Market and Capacity Expansion Opportunities and Outlook in India- 2018 Examining the market expansion trends for petrochemical industry in India and the scope of business E-REP Market

Refineries, Product Market and Capacity Expansion Opportunities and Outlook in India- 2018 Examining the market expansion trends for petrochemical industry in India and the scope of business E-REP Market

Regional Energy Trade and Refining Industry in Northeast Asia

15 th Northeast Asia Economic Forum 5-7 September 2006, Khabarovsk Russia Regional Energy Trade and Refining Industry in Northeast Asia Kensuke Kanekiyo Managing Director The Institute of Energy Economics,

15 th Northeast Asia Economic Forum 5-7 September 2006, Khabarovsk Russia Regional Energy Trade and Refining Industry in Northeast Asia Kensuke Kanekiyo Managing Director The Institute of Energy Economics,

Refinery Update. John C. Felmy Chief Economist American Petroleum Institute October 2006

Refinery Update John C. Felmy Chief Economist American Petroleum Institute Felmyj@api.org www.api.org October 2006 1 2 Diesel, gasoline & crude oil prices $3.87 $3.22 10/16/2006 Diesel (EIA) $2.50 Retail

Refinery Update John C. Felmy Chief Economist American Petroleum Institute Felmyj@api.org www.api.org October 2006 1 2 Diesel, gasoline & crude oil prices $3.87 $3.22 10/16/2006 Diesel (EIA) $2.50 Retail

PETE 203: Properties of oil

PETE 203: Properties of oil Prepared by: Mr. Brosk Frya Ali Koya University, Faculty of Engineering, Petroleum Engineering Department 2013 2014 Lecture no. (3): Classification of Crude oil 6. Classification

PETE 203: Properties of oil Prepared by: Mr. Brosk Frya Ali Koya University, Faculty of Engineering, Petroleum Engineering Department 2013 2014 Lecture no. (3): Classification of Crude oil 6. Classification

ANALYST BRIEFING FOR THE FOURTH QUARTER ENDED FEBRUARY 2017

ANALYST BRIEFING FOR THE FOURTH QUARTER ENDED 2016 22 FEBRUARY 2017 MSM Malaysia Holdings Berhad Analyst Briefing Q4 2016 22/2/2017 1 CONTENTS 01 02 03 04 05 Group Financial Highlights Performance Review

ANALYST BRIEFING FOR THE FOURTH QUARTER ENDED 2016 22 FEBRUARY 2017 MSM Malaysia Holdings Berhad Analyst Briefing Q4 2016 22/2/2017 1 CONTENTS 01 02 03 04 05 Group Financial Highlights Performance Review

Energy Economics. Lecture 3 Crude Oil Market ECO Asst. Prof. Dr. Istemi Berk

Energy Economics ECO-4420 Lecture 3 Crude Oil Market Asst. Prof. Dr. Istemi Berk istemi.berk@deu.edu.tr 1 World Fossil Fuel Consumption A Comparison btw. Coal, Oil and Gas Million Tons of Oil Equivalent

Energy Economics ECO-4420 Lecture 3 Crude Oil Market Asst. Prof. Dr. Istemi Berk istemi.berk@deu.edu.tr 1 World Fossil Fuel Consumption A Comparison btw. Coal, Oil and Gas Million Tons of Oil Equivalent

INDUSTRY OVERVIEW OVERVIEW OF THE PETROLEUM INDUSTRY AND SUPPLY CHAIN

Certain information and statistics set out in this section and elsewhere in this document are derived from various government and other publicly available sources, and from the market research report prepared

Certain information and statistics set out in this section and elsewhere in this document are derived from various government and other publicly available sources, and from the market research report prepared

OUTLINING STORAGE REGIONALLY IN AFRICA How much is sufficient and well-linked storage key to security of supply and competitive pricing?

Platts African Refining Summit 2014 OUTLINING STORAGE REGIONALLY IN AFRICA How much is sufficient and well-linked storage key to security of supply and competitive pricing? - by Gabriel Ogbechie, Managing

Platts African Refining Summit 2014 OUTLINING STORAGE REGIONALLY IN AFRICA How much is sufficient and well-linked storage key to security of supply and competitive pricing? - by Gabriel Ogbechie, Managing

Changes in Bunker Fuel Quality Impact on European and Russian Refiners

Changes in Bunker Fuel Quality Impact on European and Russian Refiners Russia & CIS Bottom of the Barrel Technology Conference 23 &24 April 2015, Moscow Euro Petroleum Consultants TABLE OF CONTENT Requirements

Changes in Bunker Fuel Quality Impact on European and Russian Refiners Russia & CIS Bottom of the Barrel Technology Conference 23 &24 April 2015, Moscow Euro Petroleum Consultants TABLE OF CONTENT Requirements

Anne Korin Institute for the Analysis of Global Security

How next generation energy can set America free from oil dependence Anne Korin Institute for the Analysis of Global Security http://www.iags.org The Institute for the Analysis of Global Security (IAGS)

How next generation energy can set America free from oil dependence Anne Korin Institute for the Analysis of Global Security http://www.iags.org The Institute for the Analysis of Global Security (IAGS)

UK Continental Shelf (UKCS) Oil and Gas Production and the UK Economy. Mike Earp

Oil and Gas Production and the UK Economy. Mike Earp") UK Continental Shelf (UKCS) Oil and Gas Production and the UK Economy Mike Earp 15 June 215 Outline Production and Reserves Expenditure, Income and Taxation Gross Value Added Trade Recent Production History

UK Continental Shelf (UKCS) Oil and Gas Production and the UK Economy Mike Earp 15 June 215 Outline Production and Reserves Expenditure, Income and Taxation Gross Value Added Trade Recent Production History

Statistical Appendix

Statistical Appendix Middle East and Central Asia Department REO Update, May 2013 The IMF s Middle East and Central Asia Department (MCD) countries and territories comprise Afghanistan, Algeria, Armenia,

Statistical Appendix Middle East and Central Asia Department REO Update, May 2013 The IMF s Middle East and Central Asia Department (MCD) countries and territories comprise Afghanistan, Algeria, Armenia,

Global Overview of Middle Distillates Supply and Demand ICE Market Forum Rotterdam, November 2012

Global Overview of Middle Distillates Supply and Demand ICE Market Forum Rotterdam, November 2012 About Petromatrix Based in Switzerland (city of Zug) Publishes a daily newsletter on oil markets Mix of

Global Overview of Middle Distillates Supply and Demand ICE Market Forum Rotterdam, November 2012 About Petromatrix Based in Switzerland (city of Zug) Publishes a daily newsletter on oil markets Mix of

For Region 5 and Region 7 Regional Response Teams Meeting April 22, 2015 St. Charles, Missouri via video/teleconference

For Region 5 and Region 7 Regional Response Teams Meeting St. Charles, Missouri via video/teleconference By Grant Nülle, Upstream Oil & Gas Economist, Exploration and Production Analysis Team U.S. Energy

For Region 5 and Region 7 Regional Response Teams Meeting St. Charles, Missouri via video/teleconference By Grant Nülle, Upstream Oil & Gas Economist, Exploration and Production Analysis Team U.S. Energy

Cosmo Oil Co., Ltd. Presentation on Results for First Quarter of Fiscal 2012 August 2, 2012 Director: Satoshi Miyamoto

Cosmo Oil Co., Ltd. Presentation on Results for First Quarter of Fiscal 2012 August 2, 2012 Director: Satoshi Miyamoto Copyright 2012 COSMO OIL CO.,LTD. All Rights Reserved. Key Points of Financial Results

Cosmo Oil Co., Ltd. Presentation on Results for First Quarter of Fiscal 2012 August 2, 2012 Director: Satoshi Miyamoto Copyright 2012 COSMO OIL CO.,LTD. All Rights Reserved. Key Points of Financial Results

1 Copyright(C) 2012 Isuzu Motors Limited All rights reserved

2012 Isuzu Motors Limited All rights reserved") FY2012 Financial Results May 10, 2012 1 Copyright(C) 2012 Isuzu Motors Limited All rights reserved Contents Ⅰ. President and Representative Director : Susumu Hosoi FY2012 Overview Ⅱ. Director Director

FY2012 Financial Results May 10, 2012 1 Copyright(C) 2012 Isuzu Motors Limited All rights reserved Contents Ⅰ. President and Representative Director : Susumu Hosoi FY2012 Overview Ⅱ. Director Director

Defining the Debate: Crude Oil Exports

Defining the Debate: Crude Oil Exports Trisha Curtis, Director of Research Upstream and Midstream Energy Policy Research Foundation, Inc. (EPRINC) Brookings Task Force February 28th, 214 About EPRINC www.eprinc.org

Defining the Debate: Crude Oil Exports Trisha Curtis, Director of Research Upstream and Midstream Energy Policy Research Foundation, Inc. (EPRINC) Brookings Task Force February 28th, 214 About EPRINC www.eprinc.org